ESRS Topic Structure: these are the Planned Changes

Overview of the new ESRS topic structure: Planned changes for 2025, impact on companies, and relevance for sustainability reports.

- The ESRS are being restructured from three tiers (topics, sub-topics, sub-sub-topics) down to two tiers, removing or integrating the most granular level.

- On 6 May 2026 the EU Commission published a draft of simplified ("revised") ESRS for consultation, cutting mandatory data points by over 60% and total data points by over 70%.

- Key changes affect all ten standards: E1 stays unchanged; E2 and E3 consolidate; E4 and E5 broaden scope; S1 and S2 merge; G1 integrates anti-corruption and animal welfare under corporate culture.

- Companies already using the ESRS should check whether removed sub-topics remain material for their specific sector and update their materiality assessment accordingly.

- The ESRS data points template helps companies track exactly which data points still apply after the restructuring.

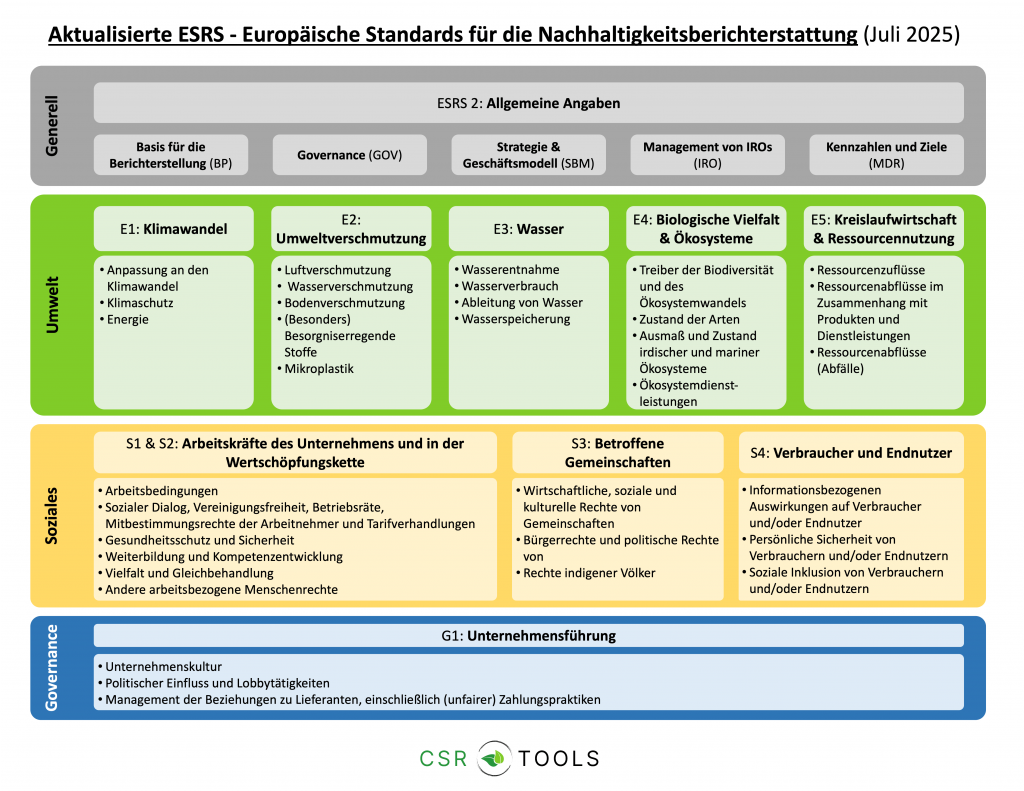

The European Sustainability Reporting Standards (ESRS) form the core of the EU's Corporate Sustainability Reporting Directive (CSRD). Previously, the structure was three-tiered:

- Topics (e.g., climate change, biodiversity, workforce),

- Sub-topics,

- Sub-sub-topics (e.g., specific aspects like child labor, water withdrawal, or animal welfare).

This level of detail offered the advantage of clear guidance but brought high complexity for many companies, especially small and medium-sized enterprises (SMEs).

Planned Changes to the ESRS Topic Structure: from Three to Two Tiers

The proposal for adapting the ESRS foresees a streamlining: in the future, there will only be topics and sub-topics. Sub-sub-topics will be removed or integrated into the higher level.

On 6 May 2026, the EU Commission published a draft of simplified ("revised") ESRS for public consultation. The key figures: mandatory data points cut by over 60%, total data points by over 70%, and estimated reporting costs per company down by over 30%. The feedback period ran until 3 June 2026. A final delegated act is expected later in 2026.

Key Changes at a Glance:

- E1 Climate Change: No changes. Focus remains on climate protection, adaptation, and energy.

- E2 Pollution: "Pollution of living organisms and food resources" is removed (too sector-specific, hardly measurable). Substance-related topics are merged.

- E3 Water and Marine Resources: Sub-sub-topics like "water consumption" become independent sub-topics. "Discharge into oceans" is removed, "water storage" is newly added. The use of marine resources will be covered in other standards in the future.

- E4 Biodiversity and Ecosystems: Drivers such as invasive species are expanded. Examples (species extinction, land degradation) are removed for more flexibility and fewer checklists.

- E5 Circular Economy: Resource inflows and outflows remain, but services are now also considered. Marine resources are moved here.

- S1 and S2 Workforce: Own employees and value chain are merged into a unified logic for HR topics.

- S3 Affected Communities: Detailed topics (housing, nutrition, safety) are integrated into broader categories.

- S4 Consumers and End-users: Data protection, child protection, access to information, etc., merge into larger blocks.

- G1 Corporate Governance: Topics such as corruption, whistleblowing, and animal welfare are no longer reported individually, but within the framework of "corporate culture."

Why are these Changes to the ESRS Topic Structure Being Proposed?

The European Commission and EFRAG aim to achieve the following with the restructuring under the Omnibus Proposal:

- Reduce complexity: Especially for SMEs who might be overwhelmed by CSRD reporting obligations, the reduction of the ESRS topic structure offers a real simplification.

- Create more flexibility: Companies should no longer tick off rigid checklists but identify relevant topics for their context. They can choose between a top-down and a bottom-up approach for identifying material topics.

- Strengthen the materiality assessment: Companies must prioritize for themselves, through the Materiality Assessment, which topics are material and thus subject to reporting.

Who is this Relevant for?

- SMEs and mid-sized companies that will no longer fall under the CSRD obligation but still wish to publish a simplified sustainability report on a voluntary basis (e.g., VSME Standard) -- fewer detailed requirements, more self-responsibility.

- Large companies that must report comprehensively under the CSRD -- they benefit from a clearer structure but must carefully assess whether removed details remain material for their industry.

- CSRD consultancies, ESG software providers (such as Materiality Master) and auditors who need to adapt their tools and processes.

The Commission draft published on 6 May 2026 is still going through the legislative process. A final adoption of the revised ESRS delegated act is expected later in 2026. Companies should familiarize themselves with the possible changes now to be prepared, especially regarding the execution of the materiality assessment and internal data processes.

Note: The adjustment of the ESRS topic structure is one of numerous proposed changes in the ESRS Set 1 Exposure Draft.

Detailed Overview of all Changes in the ESRS Topic Structure

| ESRS topic | Original sub-sub-topic | New mapping in 2025 proposal | Status / change | Note / rationale |

|---|---|---|---|---|

| E1 Climate change | Climate change mitigation | Climate change mitigation | Unchanged | |

| E1 Climate change | Climate change adaptation | Climate change adaptation | Unchanged | |

| E1 Climate change | Energy | Energy | Unchanged | |

| E2 Pollution | Pollution of air | Pollution of air | Unchanged | |

| E2 Pollution | Pollution of water | Pollution of water | Unchanged | |

| E2 Pollution | Pollution of soil | Pollution of soil | Unchanged | |

| E2 Pollution | Pollution of living organisms and food resources | Removed | Removed | No disclosure / too sector-specific |

| E2 Pollution | Substances of concern | Substances of concern (incl. very high concern) | Merged | Merged with "very high concern" |

| E2 Pollution | Substances of very high concern | Substances of concern (incl. very high concern) | Merged | Merged into "concern" |

| E2 Pollution | Microplastics | Microplastics | Unchanged | |

| E3 Water and marine resources | Water consumption | Water consumption (now sub-topic) | Moved | From sub-sub to sub-topic |

| E3 Water and marine resources | Water withdrawals | Water withdrawals (now sub-topic) | Moved | From sub-sub to sub-topic |

| E3 Water and marine resources | Water discharges | Water discharges (now sub-topic) | Moved | From sub-sub to sub-topic |

| E3 Water and marine resources | Water discharges into oceans | Removed | Removed | Covered via ESRS 1 |

| E3 Water and marine resources | Water storage | Water storage | New | Newly introduced |

| E3 Water and marine resources | Extraction and use of marine resources | Moved to E5 | Moved | Now in E5 |

| E4 Biodiversity and ecosystems (direct drivers of biodiversity loss) | Climate change | Drivers of biodiversity and ecosystem change (terrestrial and marine) | Consolidated | Marine drivers added |

| E4 Biodiversity and ecosystems | Land-use change; freshwater/sea-use change | Drivers of biodiversity and ecosystem change | Consolidated | Broader scope |

| E4 Biodiversity and ecosystems | Direct exploitation | Drivers of biodiversity and ecosystem change | Consolidated | Broader scope |

| E4 Biodiversity and ecosystems | Invasive alien species | Drivers of biodiversity and ecosystem change | Consolidated | Broader scope |

| E4 Biodiversity and ecosystems | Pollution | Drivers of biodiversity and ecosystem change | Consolidated | Broader scope |

| E4 Biodiversity and ecosystems | Other | Drivers of biodiversity and ecosystem change | Consolidated | Broader scope |

| E4 Biodiversity and ecosystems (state of species -- examples) | Species population size (example) | Removed | Example removed | Examples deleted |

| E4 Biodiversity and ecosystems | Species extinction risk (example) | Removed | Example removed | Examples deleted |

| E4 Biodiversity and ecosystems | Land degradation (example) | Removed | Example removed | Examples deleted |

| E4 Biodiversity and ecosystems | Desertification (example) | Removed | Example removed | Examples deleted |

| E4 Biodiversity and ecosystems | Soil sealing (example) | Removed | Example removed | Examples deleted |

| E4 Biodiversity and ecosystems | Ecosystem services | Ecosystem services | Unchanged | Editorial |

| E5 Circular economy | Resource inflows incl. resource use | Resource inflows | Edited | "incl. use" removed |

| E5 Circular economy | Resource outflows: products and materials | Resource outflows: products and services | Expanded | Services added |

| E5 Circular economy | Waste | Waste | Unchanged | Editorial |

| E5 Circular economy | Marine resources (from E3) | Marine resources | Moved | Integrated here |

| S1 Own workforce | Secure employment | Merged into new combined S1/S2 block "Own workforce and workers in the value chain" | Merged | S1+S2 combined |

| S1 Own workforce | Working time | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Adequate wages | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Social dialogue | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Freedom of association; works councils; rights | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Collective bargaining (incl. coverage) | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Work-life balance | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Health and safety | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Gender equality and equal pay | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Training and skills development | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Employment and inclusion of persons with disabilities | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Measures against violence and harassment | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Diversity | Merged into S1/S2 block | Merged | |

| S1 Own workforce | Child labour | Merged into S1/S2 block (other labour-related rights) | Merged | |

| S1 Own workforce | Forced labour | Merged into S1/S2 block (other labour-related rights) | Merged | |

| S1 Own workforce | Adequate housing | Merged into S1/S2 block (other labour-related rights) | Merged | |

| S1 Own workforce | Privacy | Merged into S1/S2 block (other labour-related rights) | Merged | |

| S2 Workers in the value chain | (Analogous to S1: all sub-sub-topics) | Integrated into S1/S2 combined block | Merged | |

| S3 Affected communities | Adequate housing | Economic, social and cultural rights | Consolidated | |

| S3 Affected communities | Adequate food | Economic, social and cultural rights | Consolidated | |

| S3 Affected communities | Water and sanitation | Economic, social and cultural rights | Consolidated | |

| S3 Affected communities | Land-related impacts | Economic, social and cultural rights | Consolidated | |

| S3 Affected communities | Security-related impacts | Economic, social and cultural rights | Consolidated | |

| S3 Affected communities | Freedom of expression | Civil and political rights | Consolidated | |

| S3 Affected communities | Freedom of assembly | Civil and political rights | Consolidated | |

| S3 Affected communities | Impacts on human rights defenders | Civil and political rights | Consolidated | |

| S3 Affected communities | Free, prior and informed consent (FPIC) | Rights of indigenous peoples | Unchanged | |

| S3 Affected communities | Self-determination | Rights of indigenous peoples | Unchanged | |

| S3 Affected communities | Cultural rights | Rights of indigenous peoples | Unchanged | |

| S4 Consumers and end-users | Privacy | Information-related impacts | Consolidated | |

| S4 Consumers and end-users | Freedom of expression | Information-related impacts | Consolidated | |

| S4 Consumers and end-users | Access to information | Information-related impacts | Consolidated | |

| S4 Consumers and end-users | Health and safety | Personal safety | Consolidated | |

| S4 Consumers and end-users | Security of person | Personal safety | Consolidated | |

| S4 Consumers and end-users | Protection of children | Personal safety | Consolidated | |

| S4 Consumers and end-users | Non-discrimination | Social inclusion | Consolidated | |

| S4 Consumers and end-users | Access to products and services | Social inclusion | Consolidated | |

| S4 Consumers and end-users | Responsible marketing practices | Social inclusion | Consolidated | |

| G1 Business conduct | Corporate culture | Corporate culture (incl. anti-corruption, whistleblowers, animal welfare) | Consolidated | Integrated |

| G1 Business conduct | Corruption and bribery | Corporate culture | Consolidated | |

| G1 Business conduct | Whistleblowers protection | Corporate culture | Consolidated | |

| G1 Business conduct | Animal welfare | Corporate culture | Consolidated | |

| G1 Business conduct | Political influence and lobbying | Political influence and lobbying (editorial) | Unchanged | Minor edits |

| G1 Business conduct | Supplier relationships incl. payment practices | Supplier relationships (editorial) | Unchanged | Minor edits |

Conclusion on the Updated ESRS Structure

The planned ESRS streamlining brings both opportunities and challenges for companies:

- Opportunity: Less complexity and a clearer two-tier structure reduce reporting burden, especially for smaller teams.

- Opportunity: The simplified materiality assessment makes it easier to focus on what genuinely matters for your business.

- Challenge: Existing materiality assessments should be reviewed and adapted to the new ESRS topic structure.

- Challenge: Removed sub-topics (e.g., organisms, animal welfare as a standalone topic) may still be material for specific industries and should not be overlooked.

Companies should closely follow developments, stay up-to-date via resources like the CSRD Compass Newsletter, update their materiality assessment, and verify whether removed sub-topics remain reportable in their sector.

Keep track of which ESRS data points apply to your company after the restructuring. The ESRS data points template maps all relevant data points so you can immediately see what still applies and what has changed.

Frequently asked questions about the ESRS topic structure

What does the change from three tiers to two tiers mean in practice?

Under the current ESRS, companies must navigate topics, sub-topics, and sub-sub-topics. The planned revision removes the sub-sub-topic level. Those granular details are either merged into the sub-topic level above them or dropped entirely. The result is fewer line items to assess in your materiality process and fewer potential disclosure requirements.

Are the revised ESRS already in force?

No. As of June 2026, the EU Commission published a draft for consultation on 6 May 2026. The feedback period closed on 3 June 2026. A final delegated act is expected later in 2026. Until the revised standards are formally adopted, companies subject to CSRD should continue working with the current ESRS Set 1.

Do I need to redo my materiality assessment when the new structure is adopted?

You do not need to start from scratch, but a review is necessary. Some sub-sub-topics that were previously assessed separately are now merged or removed. You need to check that your existing assessments still cover the consolidated topics correctly, and confirm that any dropped topics are genuinely not material for your sector before removing them from your report.

Which ESRS standard changes the most under the restructuring?

The social standards see the most structural change. S1 (own workforce) and S2 (workers in the value chain) are merged into a single combined block. G1 also integrates previously standalone topics such as anti-corruption, whistleblower protection, and animal welfare under a single "corporate culture" sub-topic. E1 (climate change) is the only standard that remains entirely unchanged.