- Scope 3 covers all indirect emissions along the entire value chain, often exceeding 80% of a company's total carbon footprint.

- Correct calculation follows the GHG Protocol in four steps: identify material categories, collect activity data, select emission factors, and calculate and document results.

- Organizational and system boundaries determine whether emissions fall into Scope 1/2 or Scope 3, a common source of error.

- A hybrid method combining supplier-specific data, average data, and spend-based estimates is the most practical approach for most companies.

- Under CSRD and ESRS, Scope 3 is a mandatory reporting component. Managing it well strengthens your position with investors, banks, and customers.

For a company's greenhouse gas accounting, three scopes are considered. In addition to direct Scope 1 emissions, Scope 2 covers indirect emissions from energy procurement. Scope 3 encompasses all other indirect greenhouse gas emissions along the entire value chain. In many industries, these account for over 80% of total emissions. This makes Scope 3 the decisive lever for climate strategies, investor requirements, and CSRD reporting.

This article explains why Scope 3 matters for almost all companies, how to calculate it correctly, and where the greatest potential lies.

What is Scope 3 and why does it matter?

Scope 3 includes all indirect emissions along the entire value chain. It begins with upstream activities such as the manufacturing of purchased goods and their transport, and ends with downstream activities such as the use of sold products, disposal, employee commuting, or investments.

In many industries, Scope 3 emissions account for more than 80% of the total balance. This makes it the central lever for any credible climate strategy:

- Investors and banks increasingly demand transparent Scope 3 data.

- CSRD and ESRS make Scope 3 a mandatory reporting component.

- VSME allows Scope 3 to be voluntarily reported in the Comprehensive Module.

- Supply chains are becoming central actors in decarbonization.

- Net-zero targets cannot be reached without addressing Scope 3.

Companies that manage Scope 3 emissions make better investment decisions, reduce risks, and strengthen their competitive position.

Scope 1, 2, and 3 at a glance

To categorize all GHG emissions correctly, clear boundaries are needed. The demarcation depends on the approach chosen.

| Scope | Type | Examples |

|---|---|---|

| Scope 1 | Direct emissions | Own boilers, company vehicles, refrigerant losses |

| Scope 2 | Indirect emissions from purchased energy | Electricity, district heating/cooling; market-based vs. location-based factors |

| Scope 3 | All other indirect emissions along the value chain | 15 categories split into 8 upstream and 7 downstream categories |

Key Scope 3 categories include purchased goods and services (3.1), capital goods (3.2), business travel (3.6), employee commuting (3.7), use of sold products (3.11), and leased assets (3.13).

How to calculate Scope 3 correctly: The 4-step process

The correct calculation follows the GHG Protocol, a clearly defined international standard.

Step 1: Identify material categories

Upstream and downstream emissions can cover all 15 categories, but not every category is relevant for every company. A solid materiality assessment determines which categories to prioritize. Assess based on:

- emission quantity

- your company's influence potential

- industry benchmarks

- stakeholder expectations

- data availability

This step makes Scope 3 manageable and forms the foundation of any credible calculation.

An Excel template for evaluating the GHG Protocol criteria for material Scope 3 categories. Criteria weightings are fully customizable.

Step 2: Collect activity data

Different data types are required depending on the category and data availability:

- quantities (e.g., tonnes of concrete, kWh of heat, km of travel)

- financial expenditures (spend-based)

- supplier-specific primary data

The more precise the data, the more accurate the Scope 3 results. High quality is only achievable with solid data foundations.

Step 3: Select emission factors

Documented, transparent emission factors are essential for auditors and investors. Use established sources:

- GHG Protocol (IPCC)

- ecoinvent

- ProBas

- GEMIS

Do not change data sources over time without transparent documentation. Consistent methodology ensures comparable year-on-year results.

Step 4: Calculate and document emissions

The general formula is:

Emissions (tCO2e) = Activity Data x Emission Factor

For CSRD/ESRS audits, your Scope 3 calculation must describe assumptions, disclose uncertainties, classify data quality from A to D, and maintain a consistent methodology throughout.

Which calculation method suits your situation?

Different methods are used depending on the category or data availability:

| Method | Best for | Accuracy |

|---|---|---|

| Spend-based (top-down) | Service providers, missing primary data, initial screening | Lower; good starting point |

| Average data | Transport, generic materials, early screening phases | Medium; solid middle ground |

| Supplier-specific data (bottom-up) | Emission hotspots requiring high precision | Highest; the gold standard |

| Hybrid method | Most companies, especially Scope 3 beginners | Realistic and practical |

A typical hybrid approach combines primary data for steel and concrete, average values for transport, and spend-based estimates for services.

System and organizational boundaries: A common source of error

Defining organizational boundaries (Equity Share, Operational Control vs. Financial Control) determines whether emissions fall into Scope 1/2 or Scope 3. Incorrect demarcation or inconsistent methodology application can massively over- or underestimate Scope 3. Review your boundary definitions before starting any calculation.

Typical challenges and how to solve them

Scope 3 accounting often fails due to missing supplier data, double counting, unstable baselines, lack of documentation, or unclear responsibilities.

- Establish clear division of roles from the start.

- Document all methods and assumptions.

- Conduct an annual data quality review.

- Actively involve suppliers through supplier engagement.

- Communicate results clearly via your sustainability communication.

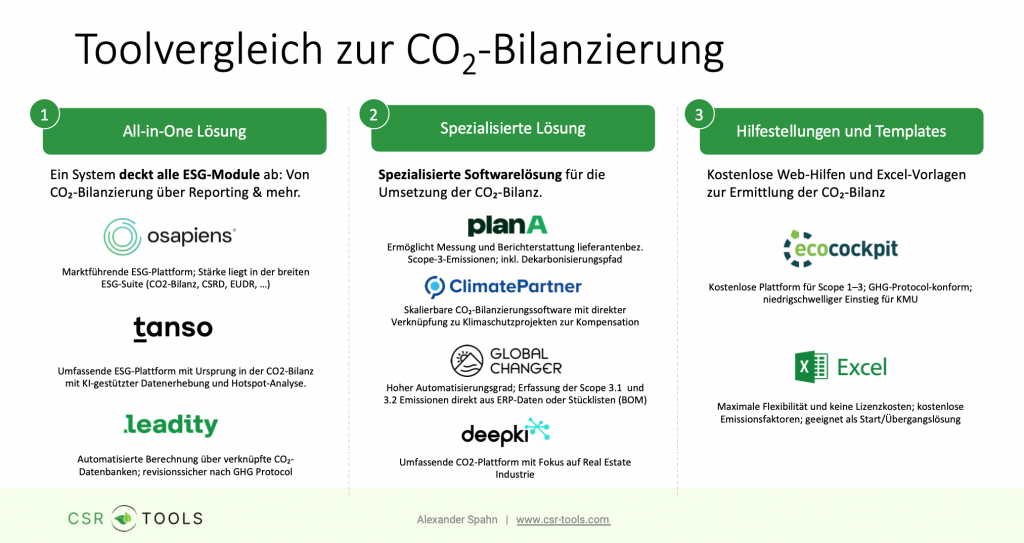

Which tools help with accounting?

For beginners:

- ecocockpit (free, GHG-compliant)

- Excel-based calculation tools from the GHG Protocol

For growing Scope 3 requirements:

- All-in-One ESG software solutions

- osapiens

- Tanso

- Leadity

- Specialized solutions for carbon footprint

- PlanA

- ClimatePartner

- Global Changer

In the CSR Tool Overview, you will find more providers and can filter by CO2 management functions.

The correct calculation remains a data and process project. Choose your tools after you have defined your methodology.

Why Scope 3 will become the most important climate metric

Scope 3 is more than a complicated number in a sustainability report. As part of the CSRD, transparent emissions data creates competitive advantages. Companies that understand and manage Scope 3 emissions gain:

- Better investment decisions based on real emissions data

- More robust climate strategies covering the full value chain

- Higher data quality in the supply chain

- Stronger position with banks, investors, and customers

Scope 3 is both a challenge and an opportunity. It is the key to any credible decarbonization strategy.

Learn to calculate your company's Scope 3 emissions step by step, including a Scope 3 materiality assessment Excel tool and practical tips for each category.

Frequently asked questions about Scope 3 and GHG accounting

What is the difference between Scope 1, 2, and 3 emissions?

Scope 1 covers direct emissions from sources your company owns or controls (boilers, company vehicles). Scope 2 covers indirect emissions from purchased electricity and heat. Scope 3 covers all other indirect emissions along the value chain, both upstream (e.g., purchased goods, transport) and downstream (e.g., use of sold products, business travel, investments).

Is Scope 3 reporting mandatory under CSRD?

Yes. Under CSRD and the ESRS, Scope 3 is a mandatory reporting component for companies that fall within scope. The reporting threshold now requires more than 1,000 employees and more than 450 million euros in net turnover, both criteria applying cumulatively under the revised rules in force since March 2026.

What is the most practical method for calculating Scope 3?

For most companies, a hybrid method works best: use supplier-specific primary data for your most significant emission hotspots, average data for categories like transport, and spend-based estimates for services where no better data is available. This balances accuracy with feasibility.

Where can I get emission factors for Scope 3?

The main sources are the GHG Protocol factor database, ecoinvent, ProBas (German Environment Agency), and GEMIS. Whichever source you choose, document it clearly and keep it consistent over time. Changing sources without documentation makes year-on-year comparisons unreliable.