ESRS

The European Sustainability Reporting Standards (ESRS) are a central component of the CSRD. Learn everything you need to know.

The European Sustainability Reporting Standards (ESRS) are a central component of the Corporate Sustainability Reporting Directive (CSRD) and define how companies in the EU must report on their sustainability performance. The ESRS aim to ensure uniform, transparent, and comparable sustainability reporting.

The standards cover comprehensive Environmental, Social, and Governance (ESG) topics and are based on international frameworks such as the GRI Standards, IFRS S1 & S2, and the TCFD. Nevertheless, there are some special features, such as double materiality.

With the European Sustainability Reporting Standards, the EU aims to ensure that sustainability information is as reliable and decision-relevant as financial reports – an important step towards promoting sustainable business models and capital flows.

Helpful Tools for Complying with the European Sustainability Reporting Standards

Word template (& PDF) for a CSRD sustainability report according to the ESRS VSME standard.

Practical and interactive workshop for a better understanding and implementation of the VSME standard.

Excel-based database with hundreds of pre-formulated Impacts, Risks & Opportunities (IROs) for efficient DMA.

1. What are the European Sustainability Reporting Standards (ESRS)?

The European Sustainability Reporting Standards are binding reporting standards for sustainability reporting by companies in the European Union. They were developed by the European Financial Reporting Advisory Group (EFRAG) on behalf of the European Commission and form the basis of the Corporate Sustainability Reporting Directive (CSRD), which has applied to large companies since 2024.

Relationship between ESRS and CSRD

The CSRD defines which companies must report on sustainability, while the European Sustainability Reporting Standards define what and how exactly must be reported. This means:

- The CSRD obliges companies to report on sustainability, replaces the previous Non-Financial Reporting Directive (NFRD), and significantly expands the circle of companies subject to reporting.

- The European Sustainability Reporting Standards are the specific reporting standards that companies must use to meet CSRD requirements. They ensure that sustainability information is collected in a detailed, uniform, and comparable manner.

In short: The CSRD makes reporting mandatory and defines which companies are affected – the ESRS provide the framework for content and methodology.

Objectives of the European Sustainability Reporting Standards

The ESRS aim to ensure that companies report comprehensively, transparently, and comparably on sustainability aspects.

Affected Companies

The ESRS apply to all EU companies subject to CSRD reporting requirements:

- Large companies that meet at least two of the following three criteria:

- Balance sheet total: over €25 million

- Net sales revenue: over €50 million

- More than 250 employees

- Capital market-oriented SMEs from 2026 (with the possibility of postponement until 2028).

In November 2024, the European Commission announced the introduction of an omnibus package in the Budapest Declaration. This CSRD Omnibus Proposal was published on February 26, 2025, and aims to better align the CSRD, the Corporate Sustainability Due Diligence Directive (CSDDD), and the EU Taxonomy, to simplify reporting obligations for companies and reduce bureaucratic hurdles.

It was also proposed to adjust the implementation deadlines and the thresholds that determine which companies are even subject to reporting requirements.

The package was then finally adopted by the EU Council in February 2026 and will enter into force 20 days after publication, i.e., on 2026-03-18.

Accordingly, under the Omnibus proposal only the following companies will be required to report:

1. From reporting year 2027 (reporting in 2028):

- more than 1,000 employees

- and more than €450 million net revenue

2. First-wave companies (“wave one”)

- Companies that were already required to report under the CSRD since 2024 but, under the new thresholds, are no longer within scope may, under certain conditions, be exempted by the Member States for the 2025 and 2026 reporting years. The corresponding national implementation is at the discretion of the Member States.

The Member States must then transpose the directive into national law.

Further European Sustainability Reporting Standards

In addition to the comprehensive ESRS, which is relevant for large companies and which is the main focus of this article, EFRAG has published two other standards:

- ESRS LSME (ESRS for Listed Small- and Medium-Sized Enterprises): The ESRS LSME standard offers simplified and proportionally adjusted reporting for small and medium-sized listed companies, while the comprehensive ESRS standard requires detailed and in-depth disclosure of all relevant sustainability aspects in accordance with the CSRD.

- ESRS VSME (Voluntary Sustainability Reporting Standard for non-listed SMEs): The ESRS VSME standard offers voluntary and significantly reduced reporting tailored to the limited resources of very small companies. We have created a helpful Word report template for the VSME standard and also compiled all reporting requirements in a clear VSME data points list.

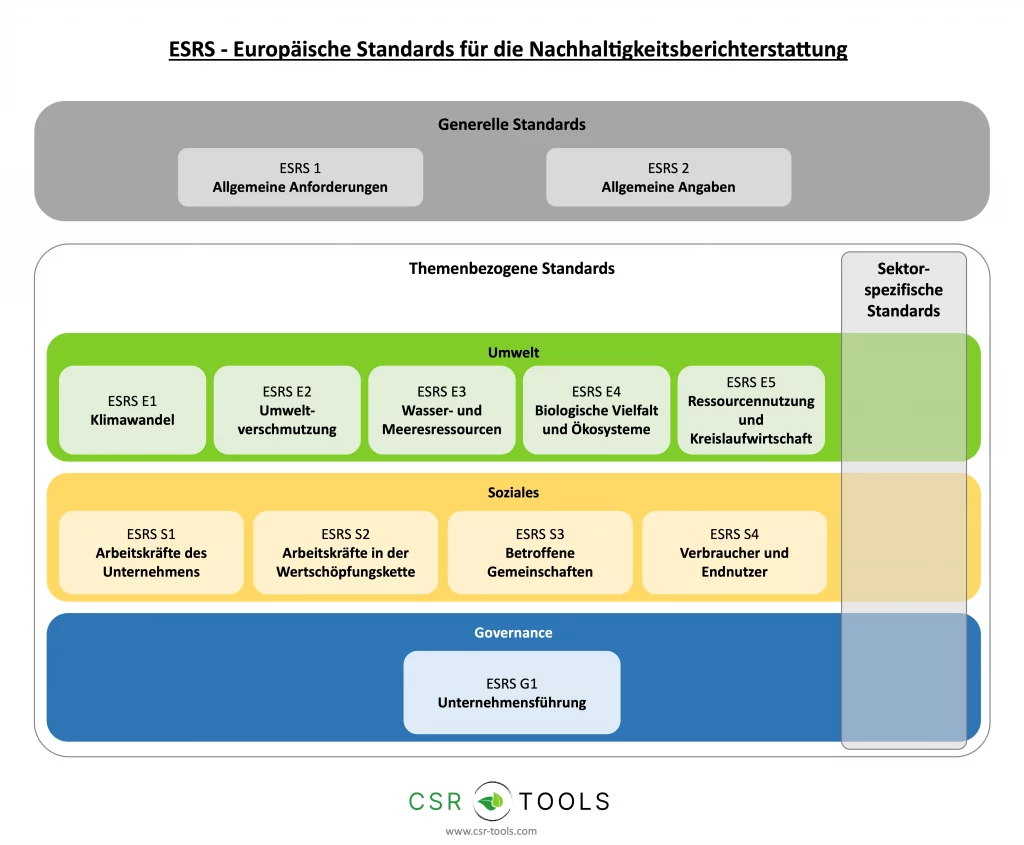

2. Structure and Standards: How are the ESRS structured?

The European Sustainability Reporting Standards are divided into various categories to ensure comprehensive and transparent reporting. They consist of general requirements, topic-specific standards for Environment (E), Social (S), and Governance (G), as well as sector- and company-specific regulations.

General Requirements: ESRS 1 & ESRS 2

The overarching standards ESRS 1 and ESRS 2 define the fundamental principles and general disclosure obligations.

ESRS 1: General requirements

ESRS 1 outlines the structure of the European Sustainability Reporting Standards, explains the requirements for their elaboration, and the underlying concepts. It also defines fundamental requirements for the preparation and presentation of sustainability-related information. The reporting period for a company’s sustainability statement must align with the reporting period for the company’s annual financial statements.

- Defines reporting principles

- Includes the concept of double materiality

- Describes coherence with other standards

ESRS 2: General information

ESRS 2 defines the requirements for information that a company must generally provide in its sustainability report for all material sustainability aspects in the following areas: Governance, Strategy, Impacts, Risks, and Opportunities (IROs), as well as metrics and targets.

- Includes fundamental reporting obligations for all companies

- Defines the structure of the sustainability report

- Sets requirements for governance, strategy, and risk management

Thematic ESRS Standards

The thematic European Sustainability Reporting Standards cover the three sustainability dimensions: Environment (E), Social (S), and Governance (G).

ESRS E1: Climate change

The ESRS E1 standard defines a company’s disclosure requirements in relation to its impact on climate change, efforts to limit global warming to 1.5 degrees in accordance with the Paris Agreement and adaptation strategies to actual and expected climatic changes.

It also contains disclosure requirements on how companies deal with their greenhouse gas emissions (Scope 1-3 emissions) and the associated risks, as well as the obligation to provide information on the company’s energy consumption and energy mix.

ESRS E2: Pollution

This section covers the company’s actual and potential impacts on air, water and soil pollution. It highlights the company’s actions and strategies to prevent and mitigate such pollution and adapt to a sustainable economy. The standard also considers the financial implications of these environmental impacts. It also includes information on substances of concern that the company produces or uses and their potential impact on people and the environment.

ESRS E3: Water and marine resources

The main objective of this standard is to enable users to recognize the actual and potential impacts of the company on water and marine resources. In addition, companies should present their measures to mitigate negative impacts and protect these resources.

The standard also requires a description of how a company adapts its business strategies in line with sustainable water use. Finally, companies must report on material risks, opportunities, and impacts arising from their relationship with water and marine resources. The standard refers to “water” as surface and groundwater, and “marine resources” as their use, return, and related activities.

ESRS E4: Biodiversity and Ecosystems

The ESRS E4 Standard aims to oblige companies to clearly present in their sustainability reports how they influence biodiversity and ecosystems. This should include both positive and negative impacts, including the company’s role in biodiversity loss. The company should also present its measures to mitigate these impacts and restore biodiversity.

The business strategy is expected to be in line with various global and EU biodiversity directives. Companies should also report on their material risks and opportunities and their financial implications in relation to biodiversity. The standard considers the company’s relationship with different habitats and ecosystems. In this context, “biodiversity” refers to the variability of organisms and their ecosystems.

ESRS E5: Circular economy

ESRS E5 is about the company’s impact on resource efficiency, the use of renewable resources and the prevention of depletion of non-renewable resources. Companies should report their actions and their results to mitigate negative impacts in this area, including measures to decouple economic growth from the use of materials.

The standard emphasizes the need to adapt business strategies to minimize waste and maximize resource efficiency. The “circular economy” describes a system that maximizes the value of products and materials by promoting their use optimization, reuse and recycling. It is designed to help companies master the transformation from a linear to a circular economy.

ESRS S1: Own Workforce

This standard stipulates that positive and negative influences of the company on its own workforce, measures taken and their results, as well as financial risks and opportunities, must be reported.

The focus is on social aspects (i) Working conditions, (ii) Equal treatment and equal opportunities for all, and (iii) Other work-related rights such as child and forced labor. Companies should explain how they address these factors and what material IROs result from them.

The ESRS S1 Standard refers only to the company’s workforce, including non-employed workers, but not to external workers in the value chain.

ESRS S2: Workforce in the value chain

The standard defines disclosure requirements for companies to make the impact of their business activities on workers in their value chain transparent. Companies should explain their approach to assessing and addressing impacts on working conditions, equal treatment & opportunities and other labor-related rights. The standard applies to all workers in the value chain who are not part of the “own workforce”.

ESRS S3: Affected communities

This area sets out how companies affect impacted communities through their business activities. Companies must explain their approach to addressing impacts on (i) communities’ economic, social and cultural rights, (ii) communities’ civil and political rights, as well as (iii) the specific rights of Indigenous Peoples, and what opportunities and risks dependency on these communities may entail.

Affected communities are individuals or groups who live or work in the same area that is or could be affected by the company’s activities or its value chain.

ESRS S4: Consumers and end users

The ESRS S4 Standard sets disclosure requirements so that report readers can identify a company’s impacts on consumers and/or end-users in the context of business, products, and services. Companies should explain their approach to topics such as (i) information-related impacts on consumers and/or end-users (e.g., privacy, freedom of expression), (ii) personal safety (e.g., health and safety, personal security, and child protection), and (iii) social inclusion of consumers (e.g., non-discrimination, access to products and services, and responsible marketing practices). Misuse of products by consumers is not part of this standard.

ESRS G1: Business conduct

The main goal of the ESRS G1 Standard is to establish clear guidelines for companies so that strategies, processes, and performance in corporate policy can be understood in the sustainability report. In particular, the following three main areas of corporate governance are considered:

(i) Corporate ethics and culture, e.g., the fight against corruption, the protection of whistleblowers;

(ii) The management of supplier relationships, especially regarding payment practices;

(iii) The way companies exert political influence and the resulting obligations, including lobbying.

Sector- and company-specific standards (future)

In addition to the general and thematic European Sustainability Reporting Standards, the EFRAG plans to develop sector-specific standards that address the particular sustainability challenges of individual sectors. These will be published in the coming years.

3. What requirements and obligations arise for companies?

The European Sustainability Reporting Standards place comprehensive demands on companies that are obliged to engage in sustainability reporting. CSRD reporting aims to increase transparency in Environmental, Social, and Governance (ESG) areas and enable better comparability.

Key Requirements of the ESRS

Companies subject to CSRD reporting requirements must disclose their sustainability information according to clearly defined specifications. The most important requirements are:

- Application of the principle of double materiality: Companies must record and evaluate both the financial impacts of sustainability topics (Financial Materiality) and their impacts on the environment and society (Impact Materiality).

- Comprehensive ESG reporting: Reports must refer to Environment (E), Social Aspects (S), and Governance (G).

- Integration into the management report: Sustainability information must in the future be part of the annual report and is thus subject to the same auditing requirements as financial reporting.

- Mandatory disclosure of key figures: Companies must provide quantitative and qualitative information on sustainability goals, strategies, and risks.

The materiality assessment as a central element

A crucial component of the European Sustainability Reporting Standards is the double Materiality Assessment (DMA). Companies must identify which sustainability topics are relevant to their business model. The DMA is often used as a strategic tool by companies. A distinction is made between two perspectives:

- Inside-out perspective: What impact does the company have on the environment and society?

- Outside-in perspective: Which sustainability risks and opportunities influence the company’s financial situation?

Only topics classified as material must be dealt with in detail in the reports.

Content Structure of ESRS Reporting

Each thematic European Sustainability Reporting Standard (e.g., ESRS E1 for climate change or ESRS S1 for own employees) is structured according to a fixed scheme comprising four central reporting areas:

- Strategy – Which sustainability aspects are relevant for the company?

- Policies – Which internal guidelines regulate these topics?

- Actions – What concrete measures does the company implement?

- Targets – What goals does the company pursue, and how is their achievement measured?

This structure ensures that companies not only report on their sustainability performance but also define clear responsibilities, measures, and targets.

Strategy

In the first section of each thematic standard, the company must demonstrate how the respective sustainability topic is linked to its overall corporate strategy. Important questions are:

- What relevance does the topic have for the business model?

- What risks and opportunities are associated with this topic?

- How does the topic affect long-term value creation?

- How are stakeholder expectations taken into account?

Here, companies must also explain how the double materiality of the topic was assessed.

Policies

Companies must state whether they have internal policies, codes of conduct, or corporate guidelines for the respective topic. These include:

- Official sustainability policies

- Governance structures for ESG topics

- Measures for compliance with regulatory requirements

- Commitments to international standards such as GRI or UN Global Compact

If no policies exist, the company must provide a justification.

Actions

This describes the concrete measures the company takes to implement its sustainability strategy. These include:

- Operational measures to reduce environmental impacts

- Programs for social sustainability (e.g., diversity, working conditions)

- Supply chain management and ESG risk management

- Investments in sustainable technologies or processes

Companies must explain what processes exist to monitor progress and minimize potential risks.

Targets and Performance Indicators

In the last section, companies must state what concrete targets they are pursuing in the respective sustainability area and how they measure them. These include:

- Clearly defined ESG targets (e.g., 30% reduction in CO₂ emissions by 2030)

- Indicators and KPIs for measuring success

- Methodology for progress review (e.g., annual reporting)

- Linkage with remuneration models or internal incentives

If no measurable targets have been set, this must be justified.

Reporting Obligations and Audit Procedures

Compliance with the European Sustainability Reporting Standards is ensured by a mandatory external audit. Companies must ensure that:

- The double Materiality Assessment has been implemented in compliance with the law and stakeholder perspectives have been considered.

- The correct data points have been disclosed and the sustainability information is comprehensible and verifiable.

- Reporting is aligned with international standards.

- The ESRS data is published in machine-readable format (XHTML, ESEF format) to enable digital evaluations.

Practical Implementation for Companies

To comply with the European Sustainability Reporting Standards, companies should implement the following steps:

- Conducting a Materiality Assessment: Evaluation of relevant ESG topics based on double materiality.

- Inventory and Gap Analysis: Determination of existing sustainability data and gaps compared to ESRS requirements.

- Optimize data management and internal processes: Introduction of suitable IT systems for collecting and analyzing ESG data.

- Integration into the annual report: Sustainability information must be integrated into the management report.

- Prepare for external audit: Ensure that reporting standards and key figures are auditable.

The ESRS place high demands on companies, but at the same time offer the opportunity to strategically integrate sustainability into the business model and position themselves for the future.

Requirements for the audit of reports

- Independent audit: Sustainability reports must be checked by external, independent auditors to ensure that the disclosed information is correct, comprehensible and comparable.

- Limited Assurance: The audit must be carried out at least at the level of “Limited Assurance”, which means that the auditors carry out a limited review of the sustainability data provided and assess its plausibility.

- Reasonable Assurance: In the long term, an extended audit obligation at the level of “Reasonable Assurance” is planned. This would include a detailed and in-depth review of the sustainability information, similar to the audit of financial reports, in order to ensure even greater reliability.

Transparency and public accessibility

- Publication in the European Single Access Point (ESAP): Companies are obliged to publish their sustainability reports centrally in the ESAP. This is intended to create uniform and transparent access to ESG data within the EU so that investors, authorities and other stakeholders can easily view and compare them.

- Digital accessibility & machine readability: Sustainability information must be digitally available and machine-readable in accordance with the XBRL taxonomy. This facilitates the automated processing, analysis and comparability of the reports, especially for financial institutions and supervisory authorities that need to efficiently evaluate large amounts of sustainability data.

4. How do the ESRS differ from other sustainability standards?

The European Sustainability Reporting Standards are not the only framework for sustainability reporting. Many companies have previously reported according to voluntary standards such as the Global Reporting Initiative (GRI), the IFRS Sustainability Standards, or the TCFD recommendations. But how do the ESRS differ from these existing frameworks, and what overlaps are there?

Comparison with other standards

| Standard | Publisher | Focus | Key Differences from ESRS |

|---|---|---|---|

| GRI (Global Reporting Initiative) | GRI | Broad ESG reporting, globally recognized | ESRS are strongly based on GRI, but are mandatory and include additional EU-specific requirements. |

| IFRS S1 & S2 (International Sustainability Standards Board, ISSB) | IFRS Foundation | Financial Materiality, focus on investors | ESRS follow the concept of Double Materiality, while IFRS only considers the financial perspective. |

| TCFD (Task Force on Climate-Related Financial Disclosures) | FSB | Climate-related financial risks | ESRS E1 adopts many TCFD requirements but goes further with binding provisions. |

| EU Taxonomy | EU Commission | Sustainable economic activities, financial market participants | The ESRS are closely linked to the EU Taxonomy and contain specific disclosure requirements for taxonomy-relevant activities. |

| SFDR (Sustainable Finance Disclosure Regulation) | EU Commission | Sustainability information for financial products | The SFDR primarily concerns financial market participants, while the ESRS affect companies across all sectors. Both regulatory frameworks complement each other. |

Are there overlaps or harmonization?

-

The European Sustainability Reporting Standards were designed to largely take existing standards into account to avoid multiple reporting. Important aspects of the GRI, IFRS, TCFD, and EU Taxonomy have been integrated into the ESRS:

- GRI as a basis: The ESRS are strongly guided by the GRI methodology for sustainability reports. Companies that already report according to GRI can retain many existing structures.

- IFRS adaptation: While the IFRS Sustainability Standards S1 & S2 primarily contain investor-relevant information, the ESRS combine financial and societal perspectives (Double Materiality).

- TCFD integration: The climate report according to ESRS E1 contains many TCFD requirements, such as the disclosure of climate-related risks and opportunities.

- EU Taxonomy and SFDR linkage: The ESRS adopt central Taxonomy criteria and ensure that companies report consistently on sustainable economic activities.

- German Sustainability Code: The DNK originally created its own standard for sustainability reporting. With the introduction of the CSRD, the DNK has transformed into a supporting service provider for the implementation of the ESRS.

What are the advantages of ESRS?

Compared to voluntary reporting standards, the European Sustainability Reporting Standards have several clear advantages:

- Binding nature: While GRI, IFRS S1 & S2, or TCFD can be used voluntarily, the ESRS are mandatory for all CSRD-obligated companies.

- Double Materiality: The ESRS require a more comprehensive analysis of a company’s impacts on the environment and society – not just financial risks.

- Uniform framework for the EU: The ESRS create a clear, legally binding reporting framework for companies operating in the EU.

- Avoidance of multiple reporting: Since the ESRS cover many international requirements, companies do not have to create several separate reports.

While companies that already report according to GRI, TCFD, or EMAS or have ISO certifications can transfer many existing contents into ESRS reporting, the Double Materiality Assessment requires a deeper engagement with ESG topics.

5. Where can I find further support for implementation?

The implementation of the European Sustainability Reporting Standards presents companies with a complex task. To make reporting efficient and compliant, there are numerous official guides, regulatory documents, and CSRD assistance. The following are central sources and contact points.

Assistance and guidelines for implementation

EFRAG (European Financial Reporting Advisory Group)

The EFRAG is primarily responsible for the development of the European Sustainability Reporting Standards. On the EFRAG website, companies can find all official documents, guidelines, and explanations on the ESRS, as well as current developments in sustainability reporting.

Guides and FAQs: EFRAG Implementation Guidelines

EU Commission

The European Commission provides extensive information on the legal requirements of the CSRD as well as on the links between the ESRS and other EU regulations (e.g., the EU Taxonomy).

Guidelines and reporting requirements: CSRD and ESRS

IFRS Foundation and ISSB (International Sustainability Standards Board)

The IFRS Foundation and the International Sustainability Standards Board (ISSB) offer comprehensive information on global sustainability standards and their relation to the ESRS. These resources are particularly useful for companies that already report according to IFRS and wish to apply the ESRS as supplementary requirements.

Global Reporting Initiative (GRI)

The GRI provides guidelines for sustainability reporting that can help companies implement ESRS requirements, especially in integrating Double Materiality.

Task Force on Climate-related Financial Disclosures (TCFD)

The TCFD provides recommendations for reporting climate-related risks. These recommendations are strongly incorporated into ESRS E1 reporting, particularly on climate risks and opportunities.

**CSR Tools

**We at CSR Tools are experts in all topics related to sustainability reporting according to CSRD and ESRS and offer numerous assistance options:

- Sustainability Report Template for SMEs (ESRS VSME)

- Excel template for carrying out the Materiality Assessment & matrix

- Data Point Mapping

- ESRS IRO Database for Double Materiality Assessment

Our self-service solutions combine pragmatic simplicity with in-depth expert knowledge and make sustainability reporting quick and effective to implement. 🚀 Discover the right CSR tools now!

6. Frequently Asked Questions (FAQ)

What are the European Sustainability Reporting Standards?

The European Sustainability Reporting Standards (ESRS) are mandatory reporting standards for sustainability reporting according to the CSRD. They define which ESG information companies must disclose.

Which companies do they apply to?

The ESRS apply to companies that fall under the CSRD reporting obligation. Implementation will be staggered:

- From 2024: Large listed companies (>500 employees).

- From 2025: All other large companies.

- From 2026: Capital market-oriented SMEs (with possible deferral until 2028).

What are the objectives of the ESRS?

The ESRS apply to large companies from the 2024 financial year. Listed SMEs have a transitional period until 2026.

What is the difference between CSRD and ESRS?

The CSRD determines who must report.

The ESRS specify what and how must be reported.

Which ESG topics do the ESRS cover?

The ESRS cover Environment (E), Social (S), and Governance (G) with specific standards on topics such as climate change, social responsibility, and corporate governance.

What does Double Materiality mean?

Companies must consider both:

- Their impacts on the environment & society (inside-out) and

- The financial risks from sustainability issues (outside-in).

How must ESRS be structured for reporting?

The reporting of each ESRS follows a uniform structure:

- Strategy – Relevance of the topic for the company

- Policies – Company policies and guidelines

- Actions – Measures and implementation strategies

- Targets – Sustainability goals and key figures

How are the ESRS related to other standards?

The ESRS are aligned with GRI, IFRS S1 & S2, TCFD, and the EU Taxonomy to avoid multiple reporting.

Is there an external audit requirement for ESRS reports?

Yes, sustainability reports must be audited by an external auditor, similar to financial reports.

Where can I find official guidelines for implementing the ESRS?

The EFRAG is primarily responsible for the development of the ESRS.

EFRAG Website: https://www.efrag.org