CSRD explained in under 100 words

In 100 words, you will receive a concise explanation of what CSRD is and for whom, as well as an insight into comparable global reporting approaches.

- The CSRD is an EU directive requiring large companies to report transparently on their social and environmental impact.

- Since 18 March 2026, reporting is mandatory only for companies with more than 1,000 employees AND more than €450m net turnover (both criteria must be met).

- The CSRD uses the European Sustainability Reporting Standards (ESRS) as its reporting framework.

- Similar sustainability reporting requirements exist globally, from the USA to Asia and Australia, though the CSRD remains the most binding framework.

- Even companies outside the EU can be indirectly affected through Scope 3 reporting requirements in their supply chains.

The Omnibus package took effect on 18 March 2026. The reporting scope has been significantly narrowed. For the most current information on who is now required to report, read our post: CSRD Omnibus – What the EU proposal means for companies.

I recently attended an expert webinar on the topic of the Corporate Sustainability Reporting Directive (CSRD). At the end of the event, one of the participants wrote in the chat "I'm still not sure what exactly CSRD is…".

Many of us know that sustainability, and sustainability reporting in particular, is currently a very hot topic. It is a topic that affects numerous companies in Germany and still generates many question marks in the minds of those responsible.

Here is our attempt to explain the CSRD simply with an analogy – in less than 100 words.

CSRD explained simply as an analogy

Think of the Corporate Sustainability Reporting Directive (CSRD) as the recipe book for corporate sustainability:

Just as a cookbook provides detailed instructions and ingredients for a dish, the CSRD specifies which "ingredients" (information) companies must include in their sustainability reports. The aim is to promote "delicious" (sustainable and socially responsible) corporate governance by providing clear and comparable "recipes" (reporting standards) for everyone. This allows "guests" (investors, stakeholders) to select and rate the "dishes" (companies) based on their "taste" (sustainability performance), encouraging the "kitchens" (companies) to develop "healthier" and "tastier" options.

Is the analogy not within your grasp? No problem! Here is an attempt to explain CSRD in under 100 words without analogy:

CSRD explained in under 100 words

The Corporate Sustainability Reporting Directive (CSRD) is an EU directive that obliges certain companies to report transparently on their social and environmental impact. The focus is on the disclosure of sustainability-related information to inform investors, regulators and the public about the sustainability performance of companies. The CSRD aims to promote sustainable investment by providing clear and comparable data and encouraging companies to disclose their sustainable development practices and policies. By improving transparency and accountability, the directive supports the EU in its efforts to achieve the Sustainable Development Goals.

If you want to understand the CSRD in detail and also the connections with the ESRS, the EU taxonomy or even the concept of double materiality, it is much more complicated. Fortunately, we have put together a guide to creating a materiality assessment and further information on double materiality assessment for you.

For which companies is the CSRD relevant?

Having explained CSRD in under 100 words, let's now look at who the regulations are relevant for.

The CSRD, with its strong focus on transparent, consistent and comparable sustainability information, is pushing EU companies to shed more light on their ESG (Environmental, Social, and Governance) efforts.

Under the Omnibus package, the reporting obligation now applies only to companies with more than 1,000 employees AND more than €450m net turnover. Both criteria must be met cumulatively. Many companies that previously expected to report under the old "2 of 3 criteria" (250 employees / €40m turnover / €20m balance sheet) are no longer in scope.

Are only German companies affected by the CSRD?

No, the Corporate Sustainability Reporting Directive is a directive of the EU Commission. Accordingly, all companies within the European Union that fulfill the requirements are affected by the CSRD. Large companies in particular, as well as companies on the capital market, will have to disclose their sustainability efforts. The CSRD can also be relevant for small and medium-sized enterprises (SMEs) in the EU if they are part of the supply chain of an obligated company.

Companies outside the EU are also affected if they conduct significant business in the EU, including a physical presence. The CSRD applies if a company has achieved a turnover (net) of 150 million euros in the EU in each of the last two consecutive years and fulfills one of the following two criteria:

- a large or listed EU subsidiary; or

- an EU branch with net sales of more than EUR 40 million in the previous financial year

A PwC CSRD study published in October 2023 reveals the progress of companies in the DACH region with the implementation of ESRS requirements and presents a surprising result regarding the preferred software solution for CSRD reporting.

Indirect impact

EU companies must not only disclose their own greenhouse gas emissions (GHG emissions) as part of the CSRD. They must also report on so-called Scope 3 emissions, i.e. the GHG emissions of the entire value chain. It is therefore to be expected that companies from the EU will increasingly require their suppliers and service providers outside the EU to provide them with information on their GHG emissions. This means that companies outside the EU may also be indirectly affected by the CSRD reporting obligation.

Not sure whether your company is in scope after the new thresholds? Use our free instant check to find out in minutes.

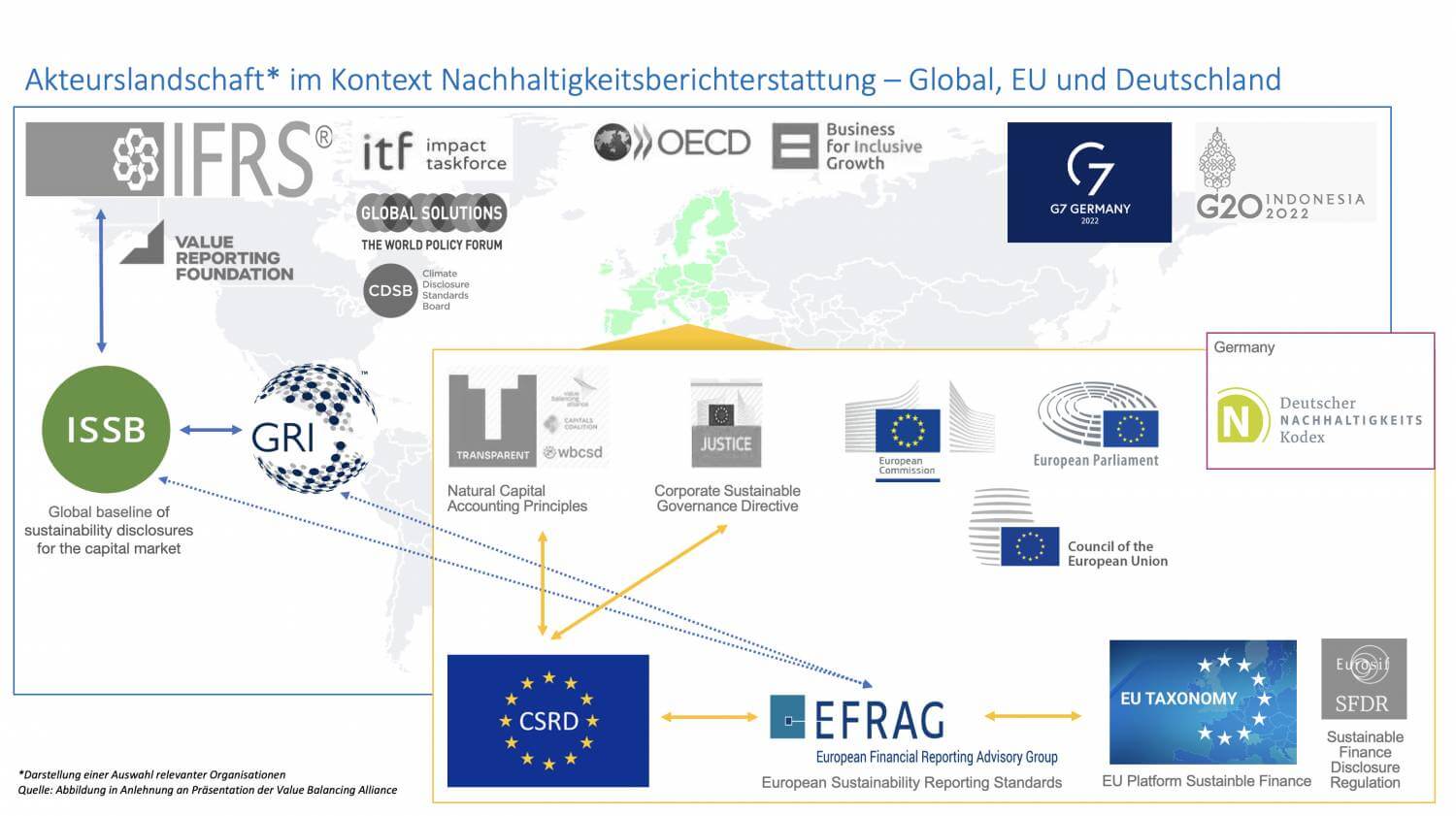

Are there similar regulations on CSRD in other countries?

Source: German Council for Sustainable Development

USA

On March 21, 2022, the US Securities and Exchange Securities and Exchange Commission (SEC) proposed regulations that would require companies (registrants) to include certain climate-related disclosures in their registration statements and periodic reports. These include information on climate-related risks that are likely to have a material impact on their business, results of operations or financial condition, and certain climate-related financial metrics in their audited financial statements. Disclosure of the registrant's greenhouse gas emissions would also be required.

The SEC's disclosure follows the GHG Protocol and the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD) and requires that the information be disclosed as part of the company's annual report on Form 10-K, but has not proposed any standards for reporting.

Other American countries

Canada follows similar principles to the USA, but offers a somewhat more structured framework with the Climate Disclosure Standards Board (CDSB), which was updated again in 2018. South American countries such as Brazil are showing increasing recognition of the importance of ESG factors with initiatives such as the Brazilian Corporate Sustainability Index.

Asia

Asia, with its diverse economic landscape, presents a range of different approaches to sustainability reporting. In countries such as Japan and Singapore, there are established frameworks such as the Japanese "Sustainability Reporting Standard", which emphasizes the importance of ESG information as a supplement to financial indicators for listed companies. Singapore offers clear guidelines for companies with its "Sustainability Reporting Guide". The Asian region shows a varied but consistently positive development towards the establishment of sustainable business practices, whereby the focus is often strongly on environmental aspects and less on social aspects compared to CSRD.

Australia

Australian companies often use the globally recognized Global Reporting Initiative (GRI) Standards for their sustainability reporting, which provides comprehensive criteria for a variety of environmental, social and governance indicators. Many companies in Australia also follow the recommendations of the Australian Accounting Standard Board (AASB), which recommends the adoption of the Task Force on Climate-related Financial Disclosures (TCFD) and thus climate-related financial information can be integrated into reporting. In addition, the AASB announced in June 2022 that it intends to develop a separate or independent set of standards that specifically address sustainability-related disclosures in the context of general financial reporting.

Comparison and convergence: A path to global sustainability?

While the CSRD provides a legally binding and standardized framework for companies in the EU, Australia, Asia and the Americas tend to show a more diverse and in some cases more voluntary approach. The European approach is stricter and more comprehensive, while standards in other regions show greater breadth and flexibility in implementation.

The differences in regional approaches to sustainability reporting reflect different economic, political and cultural contexts. However, despite these differences, there is increasing convergence towards globally harmonized reporting standards. This signals a growing global consensus on the urgent need to drive sustainable development.

In a globalizing world, the differences and similarities between regional standards could not only be instructive, but also a catalyst for the development of a universal, internationally recognized framework for sustainability reporting.

Ready to start your CSRD journey? Our Excel-based materiality analysis template helps you identify which sustainability topics are relevant for your company and meet ESRS requirements.

Frequently asked questions about CSRD

What is the CSRD in simple terms?

The CSRD (Corporate Sustainability Reporting Directive) is an EU law that requires large companies to report on their environmental and social impact. Think of it as a standardized recipe book: it tells companies which sustainability information they must disclose and in what format, so investors and other stakeholders can compare companies fairly.

Which companies must report under the CSRD?

Since 18 March 2026, reporting is mandatory for companies with more than 1,000 employees AND more than €450m net turnover. Both criteria must be met. Non-EU companies are also affected if they generate at least €150m net turnover in the EU and have either a large or listed EU subsidiary, or an EU branch with more than €40m in sales.

Are SMEs affected by the CSRD?

Most SMEs are not directly required to report under the updated rules. However, they can be indirectly affected. CSRD-obligated companies are required to report Scope 3 emissions across their value chain, which means they may ask their suppliers, including SMEs, to provide sustainability data. There is also a voluntary standard (VS, based on the former VSME standard) that SMEs can use to structure their sustainability disclosures.

How does CSRD compare to sustainability reporting in other countries?

The CSRD is the most legally binding and standardized sustainability reporting framework in the world. The USA, Asia, and Australia have developed their own frameworks, but these are often voluntary or less prescriptive. There is a growing global trend toward convergence, with frameworks increasingly aligned on climate disclosure requirements.