Double Materiality – Double Materiality Simply Explained!

Discover what Double Materiality means, why it is relevant for companies, and what a materiality matrix is.

- Double Materiality is the core concept of CSRD sustainability reporting, combining two distinct perspectives into one assessment.

- Impact materiality (inside-out) asks how your company affects people and the environment.

- Financial materiality (outside-in) asks how ESG topics affect your company's finances and strategy.

- A Double Materiality Assessment identifies which ESG topics are relevant for your report and helps prioritize strategic action.

- Under the revised Omnibus rules (in force since March 2026), only companies with more than 1,000 employees AND more than €450m net turnover are required to report under CSRD.

Sustainability is one of the defining topics of our time. For the EU to achieve its long-term goal of net-zero greenhouse gas emissions by 2050 and comply with the EU Climate Law, companies must be held more accountable.

A major step in that direction is the Corporate Sustainability Reporting Directive (CSRD) and the EU taxonomy, which oblige certain companies to prepare annual sustainability reports. At the heart of CSRD reporting is the concept of "double materiality". But what exactly does this mean and why should you care?

What is Double Materiality?

The term "Double Materiality" (also "Doppelte Wesentlichkeit" in German) refers to two perspectives of materiality in the context of sustainability reporting.

- Impact materiality (inside-out): How does your company affect the environment and society?

- Financial materiality (outside-in): How do ESG topics affect your company's financial performance, strategy, and development?

What is impact materiality (inside-out)?

Inside-out materiality focuses on the effects and consequences that your company has on external stakeholders such as society and the environment.

Examples of impact materiality based on Coca-Cola

-

Environmental impact: Coca-Cola uses significant amounts of water to manufacture its products in many regions of the world. If the company does not use these resources responsibly, this could lead to water shortages. To counteract this, Coca-Cola could introduce water treatment and reuse initiatives.

-

Social impact: If Coca-Cola employs workers in a certain country under poor working conditions, this would not only harm the workers but could also lead to public outcry and boycotts. The company could invest in fair labour practices to minimise the social impact.

-

Economic impact: In many countries, Coca-Cola supports local suppliers and small farmers by buying ingredients such as sugar or fruit from them. Paying fair prices and investing in sustainable farming methods can have a positive economic impact on these local communities.

Each of these actions, whether positive or negative, is an example of impact materiality. Companies that recognise and proactively manage the impact of their business practices are better prepared to minimise risks and seize opportunities.

What is financial materiality (outside-in)?

The outside-in perspective considers risks and opportunities arising from global or local ESG challenges that directly affect your company. These can take the form of financial impact, business interruption, or reputational damage.

Examples of financial materiality based on Coca-Cola

-

Environmental risks: Coca-Cola relies heavily on water as its main ingredient. If water shortages arise in a region where the company produces, costs could rise or production losses could occur. Proactive water management can counteract such risks.

-

Governance opportunities: Transparent reporting on ingredients, nutritional information, and business practices can increase consumer trust, leading to higher customer loyalty and ultimately better sales.

-

Social risks: A misstep in marketing, such as culturally insensitive advertising, could damage the brand and directly affect sales and share price. Effective diversity and inclusion management can lead to more innovative campaigns that appeal to a broader audience.

Paying attention to financial materiality enables companies to identify potential internal challenges and take appropriate action. A proactive approach can prevent financial losses and open up new business opportunities.

When is a topic considered "material"?

The European Sustainability Reporting Standards (ESRS) define materiality as follows:

Impact materiality:

A sustainability aspect is material from an impact perspective if it relates to the company's significant actual or potential, positive or negative impacts on people or the environment in the short, medium or long term. Material sustainability aspects include the impacts that the company has caused or contributed to, as well as the impacts directly linked to the company's own business activities, products and services through its business relationships.

Financial materiality:

A sustainability aspect is material from a financial perspective if it triggers or may trigger financial impact on the company's development, including cash flows, financial position and results of operations, in the short, medium or long term.

A Materiality Assessment can determine whether a topic is material for your company from a financial perspective (outside-in) or from an impact perspective (inside-out). We have created a guide on how you can conduct your Materiality Assessment in 4 steps.

This step-by-step Excel template takes you through the Double Materiality Assessment and automatically generates your materiality matrix.

When and why is double materiality relevant?

The CSRD specifies which companies must submit a sustainability report in accordance with the ESRS. Double materiality is a central component of this directive and is therefore relevant for all affected companies and their stakeholders.

Following the Omnibus package (in force since 18 March 2026), only companies with more than 1,000 employees AND more than €450m net turnover are required to report under CSRD. Both thresholds must be met at the same time.

Here are the key situations where double materiality becomes relevant for you:

- Strategic planning: Identify ESG risks and opportunities and integrate them into your corporate strategy from the start.

- Investor relations: More and more investors apply ESG criteria to their decisions. A proactive approach to double materiality can make your company more attractive to them.

- Risk management: Environmental and social crises can have a direct impact on your operations. Considering both materiality perspectives helps you identify those risks early.

- Reputation and brand value: Consumers increasingly choose brands that reflect their values. Taking double materiality into account can offer a significant competitive advantage.

- Stakeholder engagement: Your workforce, customers, and the communities you operate in all have expectations. Double materiality helps you engage more effectively with these groups.

Overall, double materiality is relevant if you want to build and manage a sustainable, future-oriented company. It provides a holistic view that keeps both internal and external aspects of your business activities in focus.

What is a Double Materiality Assessment?

In a double materiality assessment, both the inside-out and outside-in perspectives of your company are examined in detail. You determine the ESG topics relevant to your business, analyse both perspectives, identify opportunities and risks, and then prioritise the material topics.

Involving various stakeholders makes the analysis more robust. It should also be updated regularly, since your business environment and operating conditions can change constantly.

By conducting a Double Materiality Assessment, you can better understand and manage your ESG impacts. It also ensures that you address the topics of greatest importance to your stakeholders. This promotes more sustainable business practices and can create competitive advantages and long-term value.

The assessment can be carried out with a Materiality Assessment Excel Template or with specialised software such as Materiality Master.

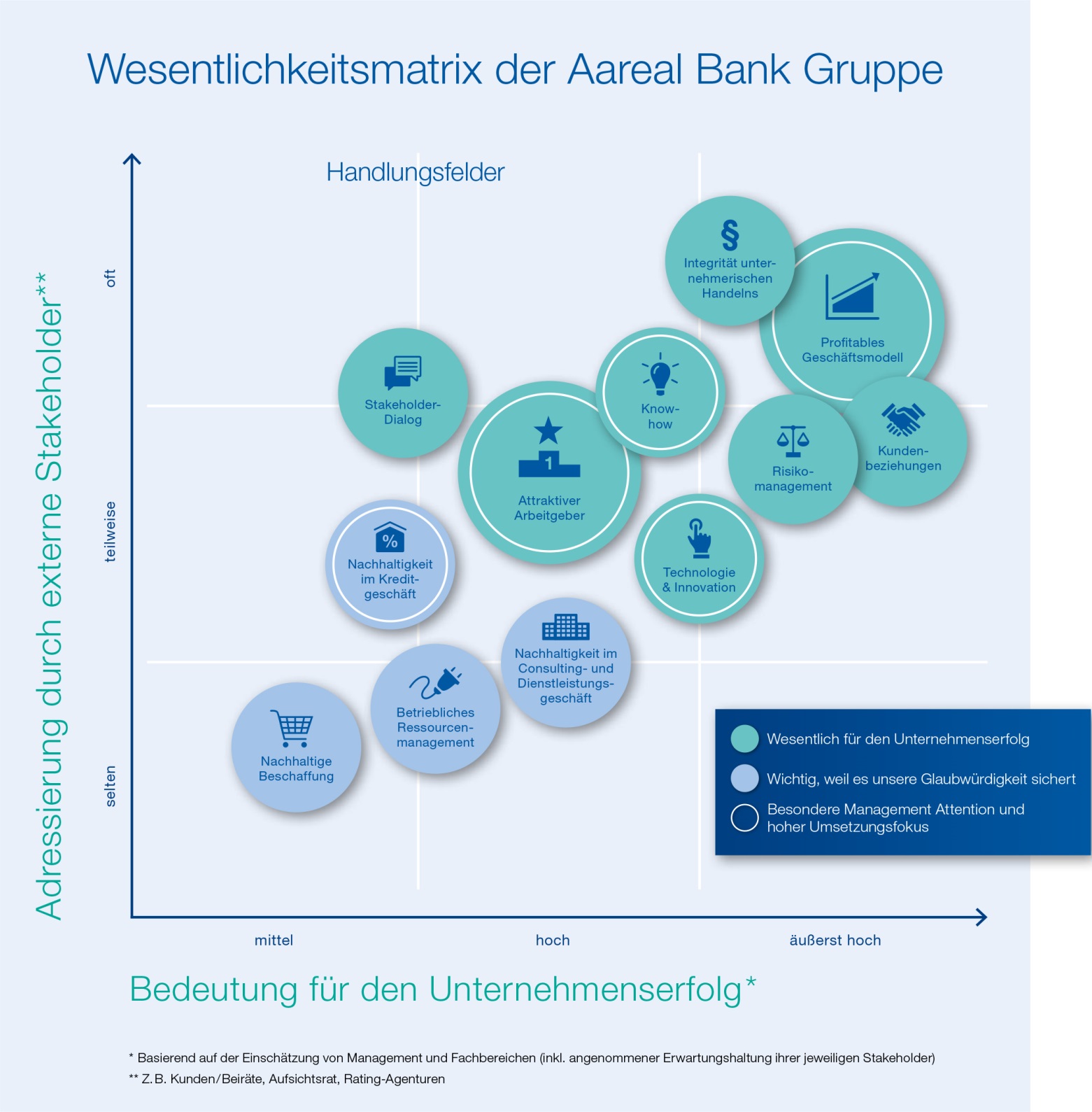

What is a materiality matrix?

A materiality matrix is a graphical tool that helps you visualise and present the results of your Double Materiality Assessment. The matrix shows the relevance and priority of ESG topics for both your company and your external stakeholders.

The matrix typically has two axes:

- Vertical axis (y-axis): The importance of the ESG topic for external stakeholders such as customers, investors, NGOs, or the local community.

- Horizontal axis (x-axis): The importance of the ESG topic for the company itself, covering financial impact, operational risks, brand image, and other internal factors.

Example of a materiality matrix

Source: www.deutscher-nachhaltigkeitskodex.de

By positioning ESG topics in this matrix, you can see at a glance:

- Which topics are important both for your company and for external stakeholders (usually in the upper right quadrant).

- Which topics matter most to external stakeholders but have less direct internal impact (top left quadrant).

- Which topics are primarily of internal relevance but are considered less important by external stakeholders (bottom right quadrant).

The materiality matrix gives you a clear overview of which ESG topics to prioritise in your strategy, reporting, and stakeholder communication. In a time of growing expectations around corporate responsibility and transparency, this tool is especially valuable.

Conclusion

Double materiality is a crucial concept that helps you shape your business strategy in a responsible and future-proof way. By addressing it, you ensure your company is on the right track from both an ethical and a financial perspective.

The Materiality Assessment Benchmark Studies by the University of Cologne and the DRSC offer good insights into how other companies approach this. And by taking double materiality seriously, you also contribute to a more sustainable and just world.

Frequently asked questions about double materiality

What is the difference between impact materiality and financial materiality?

Impact materiality (inside-out) covers how your company's activities affect people and the environment. Financial materiality (outside-in) covers how ESG risks and opportunities affect your company's finances and strategy. Together they form the basis of a Double Materiality Assessment.

Which companies must complete a Double Materiality Assessment under CSRD?

Following the Omnibus package (in force since 18 March 2026), CSRD reporting applies to companies with more than 1,000 employees AND more than €450m net turnover. Both thresholds must be met at the same time. If your company falls within scope, a Double Materiality Assessment is a required step before you can determine which ESRS data points apply to you.

How do I actually carry out a Double Materiality Assessment?

You start by identifying the ESG topics potentially relevant to your business. Then you assess each topic from both perspectives (inside-out and outside-in), involve stakeholders to validate your findings, and plot the results in a materiality matrix. A structured Excel template can guide you step by step through the process.

What is a materiality matrix and how is it used?

A materiality matrix is a chart that maps ESG topics by their importance to external stakeholders (y-axis) and to your company (x-axis). Topics in the upper right quadrant are typically the most material and should be prioritised in your sustainability report and strategy. The matrix makes it easy to communicate your priorities to investors, customers, and other stakeholders.