- The ESRS are the binding framework for sustainability reporting under the CSRD, developed by EFRAG.

- There are 12 standards covering general requirements, environmental, social, and governance topics, plus sector-specific standards in development.

- Alongside the full ESRS for large companies, there are simplified standards: ESRS LSME for listed SMEs and the voluntary ESRS VSME (being broadened into the "VS" voluntary standard) for non-listed smaller companies.

- On 6 May 2026, the EU Commission published a draft of simplified ("revised") ESRS for consultation, proposing to cut mandatory data points by over 60%.

- You can download all ESRS as a PDF from the European Commission website in 23 languages.

What are the European Sustainability Reporting Standards?

The European Sustainability Reporting Standards, or ESRS for short, mark a milestone in Europe's efforts to increase transparency and consistency in sustainability reporting (CSRD). Born out of pressure from public opinion, investor demands and the need to meet global climate targets, these standards provide a consistent basis for assessing and reporting companies' environmental, social and governance (ESG) performance. These standards were defined by EFRAG, the European Financial Reporting Advisory Group, which is also responsible for defining the International Financial Reporting Standards (IFRS) in addition to the ESRS.

The main elements of the ESRS include:

- 12 ESRS guidelines: These relate to specific information that must be included in reports to provide a clear overview of a company's sustainability efforts.

- Comparability: The standards ensure that data is comparable across different companies and sectors.

- Clarity and consistency: With the ESRS, stakeholders can be sure that the information is recorded and presented according to a defined, consistent framework.

Is there only one ESRS standard?

In addition to the comprehensive ESRS, which is relevant for large companies and which is the main focus of this article, EFRAG has published two other standards:

- ESRS LSME (ESRS for Listed Small- and Medium-Sized Enterprises): The ESRS LSME standard offers simplified and proportionally adjusted reporting for small and medium-sized listed companies, while the comprehensive ESRS standard requires detailed and in-depth disclosure of all relevant sustainability aspects in accordance with the CSRD.

- ESRS VSME (Voluntary Sustainability Reporting Standard for non-listed SMEs): The ESRS VSME standard offers voluntary and greatly reduced reporting that is geared to the limited resources of very small companies.

The VSME is being broadened into the "VS" (Voluntary Standard), expected as a delegated act later in 2026. It will be based on the VSME (EFRAG, December 2024) with small content adjustments. The VS will apply not only to SMEs but also to non-SMEs with fewer than 1,000 employees (or under €450m turnover) that fall outside the CSRD scope.

A ready-to-use Word template for your VSME sustainability report. Structured, practical, and adapted to the EFRAG standard.

Why are the European Sustainability Reporting Standards important for Europe?

The importance of the ESRS goes far beyond mere reporting obligations. They are part of the Corporate Sustainability Reporting Directive (CSRD) and a key instrument that helps Europe consolidate its role as a pioneer in sustainability and responsible business conduct.

With the "European Green Deal", the European Union has an ambitious action plan to make Europe the first climate-neutral continent by 2050. To achieve this, European countries must reduce their net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. The energy industry (37%) and industry in Germany (20%) will be responsible for over half of Germany's greenhouse gas emissions, so it is clear that companies must be held accountable to achieve these ambitious targets.

The EU Taxonomy and the ESRS provide companies with clear guidance on what information they should disclose and how it should be presented. This makes it easier for regulators to monitor progress towards the Green Deal targets and ensure that companies are doing their part.

The data provided by ESRS can also be used to assess the impact of the Green Deal on the European economy, identify potential barriers and take appropriate support measures.

In short, the Green Deal outlines the "what" and "why" for a more sustainable Europe. EFRAG's ESRS provide the "how" by delivering clear, consistent and comparable data on companies' sustainability efforts.

What is particularly relevant for companies with regard to ESRS?

How are the European Sustainability Reporting Standards structured?

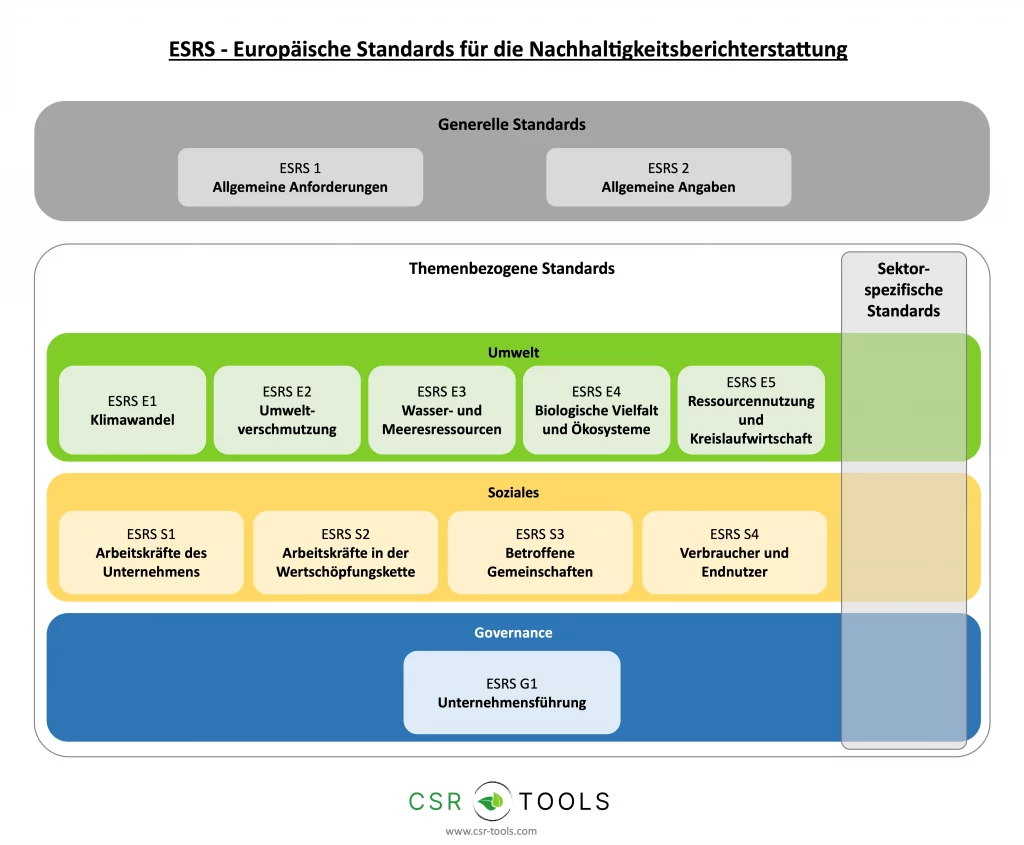

There are three categories of ESRS:

- General standards

- Thematic standards (environmental, social and governance standards)

- Sector-specific standards (affected industries)

General standards

The general standards "ESRS 1 General Requirements" and "ESRS 2 General Disclosures" apply to sustainability aspects covered by topic-specific and sector-specific standards.

They describe the general requirements for a sustainability report (such as structure and presentation) as well as the general disclosure obligations regarding the company's material sustainability aspects. Whether a topic is considered material for a company is determined by the principle of "double materiality". We have summarized the materiality assessment process in 4 steps in a separate article.

Step-by-step Excel template for your double materiality assessment. Automatically generates your materiality matrix.

Topic-related standards

The topic-related standards deal with specific sustainability topics and are divided into topics and sub-topics, and where applicable further sub-sub-topics. They may specify special requirements that go beyond and supplement "ESRS 2: General Disclosures". These specific requirements must also be followed by companies.

Sector-specific standards

Sector-specific standards apply industry-wide and address aspects such as impacts, opportunities and risks that are not sufficiently considered in topic-specific standards. They offer a deep insight into the most important topics in an industry and promote greater comparability between companies.

In January 2024, EFRAG announced that the introduction of sector-specific ESRS will be postponed by 2 years until June 2026, including sustainability reporting by companies from third countries. Sector-specific standards are planned for the following industries: Oil and gas; Coal, quarrying and mining; Logistics and road transport; Agriculture, farming and fishing; Automotive and motor vehicles; Energy production and utilities; Food and beverages; Textiles, accessories, footwear and jewelry.

What are the twelve ESRS standards?

| Standard | Name | Short description |

|---|---|---|

| ESRS 1 | General requirements | Sets out the structure of the ESRS, drafting requirements, underlying concepts and fundamental requirements for the preparation and presentation of sustainability-related information. |

| ESRS 2 | General information | Defines requirements for information a company must provide on all material sustainability aspects: governance, strategy, management of impacts, risks and opportunities, and key figures and targets. |

| ESRS E1 | Climate change | Covers a company's impact on climate change, efforts to limit global warming to 1.5°C, adaptation strategies, greenhouse gas emissions (Scope 1-3) and energy consumption. |

| ESRS E2 | Pollution | Covers actual and potential impacts on air, water and soil pollution, including substances of concern, actions to prevent and mitigate pollution, and the financial implications. |

| ESRS E3 | Water and marine resources | Requires disclosure of actual and potential impacts on water and marine resources, measures to mitigate negative impacts, sustainable water use strategies, and material risks and opportunities. |

| ESRS E4 | Biodiversity and ecosystems | Requires companies to report how they affect biodiversity and ecosystems (both positive and negative), including measures to mitigate impacts and restore biodiversity. |

| ESRS E5 | Circular economy | Covers resource efficiency, use of renewable resources and prevention of depletion of non-renewable resources, waste minimisation, and decoupling economic growth from material use. |

| ESRS S1 | Own workforce | Covers positive and negative influences on the company's own workforce: working conditions, equal treatment and opportunities, and other labour-related rights. |

| ESRS S2 | Workforce in the value chain | Defines disclosure requirements for a company's impact on workers in its value chain who are not part of the "own workforce". |

| ESRS S3 | Affected communities | Sets out how companies impact affected communities: economic, social and cultural rights; civil and political rights; specific rights of indigenous peoples. |

| ESRS S4 | Consumers and end users | Covers a company's impact on consumers and end users regarding information-related impacts, personal safety, and social inclusion. |

| ESRS G1 | Business conduct | Provides guidelines on corporate ethics and culture, management of supplier relationships (especially payment practices) and political influence and lobbying. |

Can I download the European Sustainability Reporting Standards as a PDF?

Yes, the European Sustainability Reporting Standards (ESRS) are available as a PDF download in 23 languages on the website of the European Commission. The version published on July 31, 2023 is available behind the "Annex C(2023)5303". We also provide a direct link to download the ESRS in German. Note that the document comprises 282 pages and is not particularly user-friendly.

Note: The translation into German is not yet final and may cause additional ambiguities that are better represented in the English version. It is therefore advisable to refer to the English version if in doubt.

EFRAG has published a list of all ESRS data points as an Excel file as well as further CSRD guidance to support companies in implementing the directive.

The complete list of ESRS data points as a structured Excel file. Helps you plan your reporting scope and track mandatory disclosures.

Are the ESRS standards final?

Yes, the first set of ESRS entered into force on July 31, 2023, when the Commission published the Delegated Act. After receiving over 600 responses and comments, the standards were revised and simplified once more before publication. They set binding criteria for sustainability reporting in the EU for the first time. Companies obliged to report under the CSRD must comply with these standards.

On 6 May 2026, the EU Commission published a draft of simplified ("revised") ESRS for consultation (feedback period until 3 June 2026). Key proposals include:

- Mandatory data points cut by over 60%

- Total data points reduced by over 70%

- Reporting costs per company reduced by over 30%

- Shorter and clearer structure with new flexibilities

- Simplified materiality assessment

The final revised ESRS are expected later in 2026.

Structure of the ESRS sustainability statement

ESRS requires companies to divide their sustainability statement into four parts:

- General information

- Environmental information

- Social information

- Governance information

As the information in the individual sections is not necessarily mutually exclusive, the company may refer to information already provided in another section to avoid duplication.

The information provided in the sector-specific ESRS is organized by reporting area and, where applicable, by sustainability topic. If the company provides material company-specific information, it presents it together with the most relevant non-sector-specific and sector-specific disclosures.

Source: Appendix 1 "European Sustainability Reporting Standards (ESRS)"

When presenting sustainability data, it must be possible to distinguish between information required by the ESRS and other data contained in the management report. In addition, the format of the CSRD sustainability report must be accessible to both human readers and machine-readable systems.

There are numerous software solutions that can support the creation of a sustainability report. A PwC study presents the preferred tools.

European Sustainability Reporting Standards: Conclusion and outlook

The introduction of the ESRS marks a turning point in the way European companies report on their sustainability initiatives. These standards are a tool for transparency and responsibility, and can also serve as a catalyst for positive change in the business world. The ESRS are an elementary component of the CSRD and a relevant building block for achieving the goals of the Green Deal.

By following these guidelines, companies can improve their own sustainability efforts, build trust with stakeholders, increase their attractiveness to financial investors and strengthen their market position. Overall, the introduction of the ESRS demonstrates Europe's commitment to a more sustainable future and sets a benchmark for other regions around the world.

Frequently asked questions about ESRS

What is the difference between ESRS, CSRD, and EFRAG?

The CSRD is the EU directive that makes sustainability reporting mandatory for large companies. The ESRS are the technical standards that define exactly what must be reported. EFRAG (European Financial Reporting Advisory Group) is the body that develops and maintains the ESRS on behalf of the European Commission.

Which companies must report under the ESRS?

Since 18 March 2026, the CSRD reporting obligation applies to companies with more than 1,000 employees AND more than €450m net turnover (both criteria must be met). Companies that do not meet these thresholds are not required to report but may use the voluntary VSME standard (being broadened into the "VS" Voluntary Standard).

Will the ESRS change in 2026?

Yes. On 6 May 2026, the EU Commission published a draft of revised, simplified ESRS for public consultation. The proposal would cut mandatory data points by over 60% and reduce total data points by over 70%. The final revised ESRS are expected later in 2026 as a delegated act.

Where can I find practical help for ESRS implementation?

EFRAG provides the ESRS data points as an Excel file and further CSRD guidance. For your double materiality assessment, a step-by-step materiality analysis template can significantly speed up the process.