- Sustainability is a strategic success factor, driven by the CSRD, rising investor expectations, and market pressure.

- Developing a sustainability strategy follows four phases: analysis, formulation, implementation, and monitoring.

- Double materiality is the core analytical tool, revealing both financial risks and your company's impact on the environment and society.

- As of 18 March 2026, CSRD reporting is only mandatory for companies with more than 1,000 employees AND more than €450m net turnover.

- Companies outside the CSRD scope can voluntarily report using the VS (Voluntary Standard), which is based on the VSME.

Sustainability is no longer a voluntary commitment, but a strategic success factor for companies. With the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS), the requirements for companies to systematically record and report their environmental, social and governance (ESG) aspects are increasing. Developing a sustainability strategy means much more than just compliance. It can make companies more resilient and competitive in the long term.

This article shows how companies develop a future-oriented sustainability strategy and which key concepts, such as double materiality, the Materiality Model Canvas, or transformation premiums, play a role. We also examine how disruption, ESG reporting and stakeholder expectations influence corporate strategy, and what practical measures companies should take now.

Drivers for the development of a sustainability strategy

The need to develop a sustainability strategy is shaped by various external and internal drivers. Companies that respond to these developments early on secure competitive advantages, minimize risks and benefit from long-term resilience.

1. Regulatory requirements and reporting obligations

The EU Green Deal, which includes the CSRD and the EU taxonomy, sets new standards for sustainable business.

- CSRD (Corporate Sustainability Reporting Directive): Companies must record detailed ESG data and report in accordance with ESRS standards.

- EU taxonomy: A standardized classification system that defines which economic activities are considered environmentally sustainable and contribute to EU climate targets.

The Omnibus package raised the thresholds significantly. Reporting is now only mandatory for companies with more than 1,000 employees AND more than €450m net turnover (both criteria must apply cumulatively). Companies that adapt early avoid fines, reputational risks and the costs of last-minute implementation.

2. Rising expectations of investors and financial markets

Capital markets are increasingly favouring sustainable business models. ESG criteria feed into company valuations and influence credit conditions, investor relations and stock market assessments. Companies with a clear sustainability strategy benefit from green financing models, better ESG ratings and access to sustainability-oriented funds.

3. Market and competitive pressure through transparency

Customers, business partners and suppliers are increasingly demanding sustainable products and business practices. The CSRD and its ESG reporting obligations create unprecedented transparency. Companies must disclose their social and environmental impact, not just financial figures.

- Greenwashing becomes impossible: companies must provide credible evidence of sustainable measures

- Stakeholder demands are rising: investors, customers and employees want clear sustainability strategies

- Sustainability as a purchasing criterion: ESG certifications and CO2 targets are becoming standard in many industries

Companies that do not actively integrate sustainability into their strategy will be forced to rethink by market changes. Those who act early can turn disruption into opportunity.

4. Cost factor and resource efficiency

The costs of environmental and social impacts are rising and increasingly affecting business model profitability.

| Driver | What it means for companies |

|---|---|

| CO2 pricing | Companies pay for emissions, e.g. through EU emissions trading |

| Scarcity of raw materials | Sustainable materials are becoming more expensive; recycling models more attractive |

| Supply chain requirements | Laws such as the German Supply Chain Act (LkSG) and CSDDD require compliance with human rights and environmental standards |

A sustainable transformation helps to increase energy efficiency, apply circular economy models and reduce costs over time. Companies with ESG initiatives avoid financial burdens from CO2 taxes and environmental regulations.

5. Employer branding and securing skilled workers

Sustainability is a decisive factor for employer attractiveness. Especially for younger generations, clear ESG commitments are an important criterion when choosing a job. Companies with a strong sustainability strategy attract qualified talent, improve retention and strengthen their corporate culture.

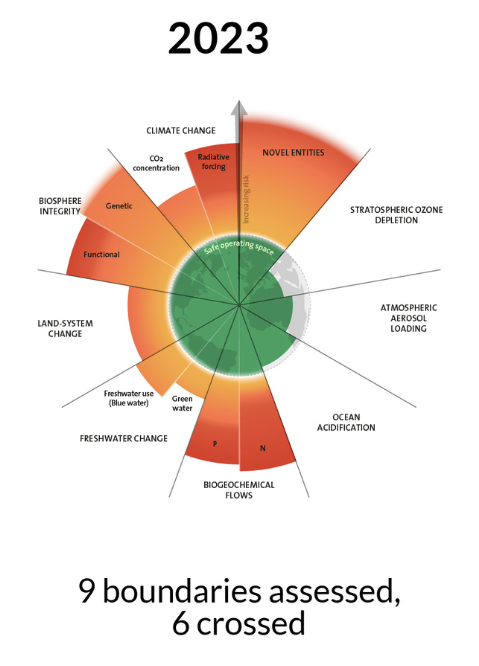

6. Planetary boundaries

The planetary boundaries define the ecological limits within which humanity can operate without destabilizing the ecosystem. Areas such as climate change, freshwater use and biodiversity have already been critically exceeded.

Companies must adapt their business models to these ecological limits, as resource scarcity, stricter environmental regulations and social pressure are making sustainable business a necessity.

7. Disruption as a driver of corporate sustainability

A sustainability strategy is increasingly an economic success factor, as disruptive changes force companies to adapt their business models. Companies that initiate a sustainability-oriented transformation early can minimize regulatory risks and exploit innovation potential.

The Innovator's Dilemma

Clayton Christensen's concept of the innovator's dilemma describes how established companies are often reluctant to adapt to new market conditions and are overtaken by more agile, innovative competitors.

Companies that see sustainability as an obligation rather than an opportunity risk being outpaced by more sustainable competitors. Companies such as Tesla and Beyond Meat have challenged traditional industries with sustainable innovations.

Companies should develop a sustainability strategy and invest in sustainable innovations before regulatory or market changes force them to do so.

Developing a sustainability strategy: The most important steps

Phase model of strategy development

Developing a sustainable corporate strategy can be divided into four core phases:

- Analysis and target definition: Analyse your external and internal environment, identify ESG risks and opportunities, and carry out a double materiality assessment to prioritize relevant sustainability issues.

- Strategy formulation and integration: Link sustainability goals to the corporate strategy, develop sustainable business models where needed, and identify investment and funding opportunities.

- Implementation and reporting: Integrate sustainability measures into corporate processes, use ESG software for data collection, and enable CSRD-compliant reporting.

- Monitoring and further development: Measure ESG performance regularly, conduct stakeholder dialogues, and adapt the strategy to new regulatory and market developments.

Phase 1: Analysis and target definition

Before developing an effective sustainability strategy, you need a comprehensive analysis of your internal and external environment. This means understanding global megatrends, regulatory requirements and market changes, and comparing them with your own business risks and opportunities.

A. External environment analysis

Start by examining general trends and external factors.

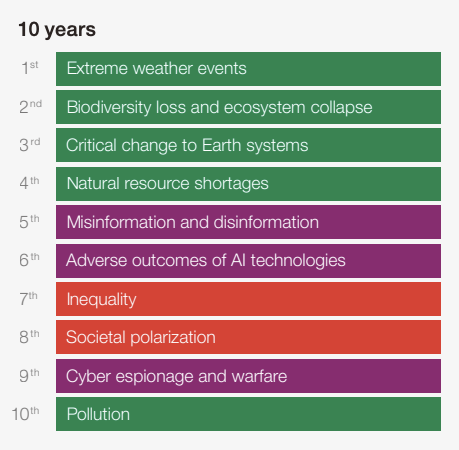

The WEF Global Risk Report

The Global Risks Report of the World Economic Forum (WEF) shows that environmental and climate risks occupy the top positions among the ten most serious global risks.

- Climate change and extreme weather events

- Loss of biodiversity and ecosystems

- Critical changes to the earth system

- Scarcity of natural resources

- Environmental pollution

Companies that do not take sustainability into account in their corporate strategy are increasingly confronted with regulatory, financial and market risks.

In addition to the Global Risk Report, reviewing the planetary boundaries helps you recognize whether your company depends on ecosystem services that may disappear in future, or whether you have negative environmental impacts in these areas.

B. Internal analysis for the sustainability strategy

Double materiality as a strategic analysis tool

The double materiality assessment is the central concept of CSRD and covers two perspectives:

A logistics company, for example, must analyze the financial impact of climate change on supply chains, and also disclose its own emissions along the value chain. Companies should see the double materiality assessment as a strategic tool, not just a compliance task. It should definitely be taken into account when developing your sustainability strategy.

Sustainable business models as a success factor

Sustainability is increasingly a driver of innovation for new business models. Companies can create added value for the environment, society and the economy through sustainable approaches.

- Dematerialization: Products offered with fewer raw materials or digitally (e.g. Spotify and Netflix replacing physical media)

- Green Razor and Blade: Sustainable products with reusable consumables (e.g. Fairphone with replaceable components)

- Circular economy: Products offered as a service rather than sold (e.g. Philips lighting as "Product-as-a-Service")

- Sharing economy: Products and services shared rather than owned (e.g. ShareNow car sharing)

- Impact models: Business models that actively solve social or ecological problems (e.g. Too Good To Go)

C. Other tools and frameworks for business analysis

A well-founded internal analysis identifies existing strengths, weaknesses and sustainability potential.

| Tool | What it covers |

|---|---|

| SWOT analysis | Identifies strengths (e.g. existing ESG programs), weaknesses (e.g. lack of sustainability expertise), opportunities (e.g. green financing) and risks (e.g. new ESG regulations) |

| PESTEL analysis | Examines external factors such as political (EU taxonomy, CSRD), economic (CO2 pricing, ESG financing) and technological developments (green innovations, digital ESG tools) |

| Five Forces analysis | Helps you understand how sustainability influences competition through changing customer requirements, new market entrants or regulatory pressure |

Phase 2: Strategy formulation and integration

A successful sustainability strategy must be more than a mandatory reporting exercise. You should strategically integrate sustainability with your business strategy to realize long-term benefits. Key concepts such as double materiality, the Materiality Model Canvas and sustainable business models help integrate sustainability into the corporate strategy in a targeted way.

A. The Materiality Model Canvas

The Materiality Model Canvas (based on the Business Model Canvas) helps companies combine sustainability with strategy and business model. It provides:

- A structured overview of relevant ESG topics

- A link between strategic opportunities and sustainability requirements

- A clear presentation as a basis for strategy development and for convincing decision-makers

A company in the retail sector can use the model to show how it can increase both environmental impact and customer satisfaction through sustainable packaging. Companies should use the Materiality Model Canvas to integrate sustainability into business decisions at an early stage.

B. Developing a sustainability strategy

An effective sustainability strategy should clearly define which ESG goals you are pursuing, which measures are required, and how progress is measured.

What belongs in a sustainability strategy

| Element | Description |

|---|---|

| Vision and strategic objectives | How does sustainability contribute to the corporate strategy? |

| Key ESG topics and fields of action | Which sustainability topics are relevant (e.g. CO2 reduction, circular economy, social standards)? |

| Key figures and success indicators | How is target achievement measured (e.g. reducing CO2 by X%, increasing recycling rate to Y%)? |

| Governance and responsibilities | Who is responsible for implementing and managing the sustainability strategy? |

Practical examples of successful sustainability strategies

Netflix transformed its business model through dematerialization, switching from physical DVD rental to digital streaming. By eliminating physical media, transportation and storage, Netflix reduced resources and emissions while creating a scalable, sustainable business model.

Unilever has consistently aligned its corporate strategy with the SDGs and integrated a program to reduce plastic and CO2 emissions.

Holcim is striving for sustainable transformation of the construction industry through CO2-reduced concrete and circular economy approaches.

A successful sustainability strategy is a key lever for growth, innovation and risk management. Sustainability should not be an add-on, but an integral part of corporate strategy.

C. Integrating the sustainability strategy

A sustainability strategy can only succeed if it is closely interlinked with the business strategy. Companies must understand sustainability as an economic value driver and integrate ESG goals into core processes, investment decisions and innovation strategies.

This means linking sustainability goals to financial KPIs, anchoring them in management structures, and incorporating them into strategic planning. Successful companies no longer view sustainability as a separate initiative, but as a new way of doing business that ensures long-term stability and competitiveness.

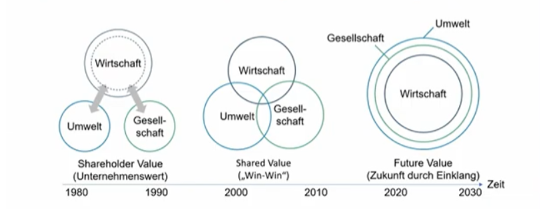

Sustainable corporate governance: from shareholder value to future value

The understanding of sustainable corporate management has changed significantly in recent decades.

Source: Prof. Dr. Thomas Wunder

| Model | Mindset | Time horizon | Handling externalities |

|---|---|---|---|

| Shareholder value (1980s-90s) | "What can my company do for shareholders?" | Short-term quarterly or medium-term return targets | Sustainability only if it directly affects company value |

| Shared value (2000s) | "What can sustainability do for my company?" | Short to medium term, depending on business case | Only where it fits the "win-win" logic |

| Future value (today) | "What can my company do for sustainability?" | Long-term competitiveness and viability | Sustainability is central: avoid or regenerate damage to environment and society |

Phase 3: Implementation and reporting

Once the sustainability strategy is formulated, the implementation phase involves translating goals into measures and integrating them into day-to-day operations.

A. Translating the strategy into concrete measures

A sustainability strategy remains ineffective if not integrated into day-to-day business through concrete measures. Companies must derive clear operational steps from defined ESG goals and KPIs to achieve measurable progress.

| ESG goal | Example measures |

|---|---|

| CO2 reduction | Switch to renewable energies, optimise logistics, promote climate-friendly mobility |

| Resource efficiency | Introduce circular economy models, sustainable procurement, waste reduction |

| Social responsibility | Diversity programs, human rights training in the supply chain, fair working conditions |

B. Sustainability key figures and performance measurement

Progress must be monitored regularly. Define clear KPIs to measure the impact of your measures.

- CO2 reduction in %

- Share of renewable energies

- Recycling and circular economy rate

- Diversity and equality indicators

Regular progress checks and adjustments are essential to ensure that KPIs are achieved.

C. Anchoring the sustainability strategy in corporate processes

- Integration into business processes: Sustainability goals must be embedded in all relevant areas, from product development and procurement to HR and financial planning.

- Using technology and innovation: Digital solutions for CO2 monitoring or the circular economy support operational implementation.

- Employee participation and change management: Sustainability can only be implemented successfully if it is anchored in corporate culture. Training, incentive systems and sustainable benefits promote acceptance.

D. Sustainability reporting and CSRD compliance

The CSRD requires companies to systematically disclose their sustainability performance. This covers not just ESG indicators, but also the underlying strategy. Companies must explain how sustainability is integrated into their business strategy, what goals they pursue, and what measures they implement.

- Data quality and digitalisation: Use CSRD software for precise data collection and automated reporting

- Transparency and credibility: Clear link between strategy, measures and results, avoiding greenwashing

- Stakeholder communication: Integrate sustainability strategy into annual reports, investor relations and corporate communications in an understandable way

As a result of the Omnibus package, many companies will fall outside the mandatory CSRD scope (fewer than 1,000 employees or under €450m turnover). Many will choose to report voluntarily using the VS (Voluntary Standard), which is based on the VSME standard published by EFRAG in December 2024 and is being broadened to cover all companies outside the CSRD scope. If you are not yet familiar with the VSME, our VSME workshop may be of interest.

Reporting outside the CSRD scope? Our VSME Word template provides a ready-to-use structure for your voluntary sustainability report.

Phase 4: Monitoring and further development

A successful sustainability strategy is not a static concept, but a dynamic process that must be regularly reviewed and developed further. Companies should continuously measure how effective their sustainability measures are and adapt their strategy to new regulatory requirements and market changes.

A. Regular ESG performance measurement and optimisation

To ensure that ESG targets are achieved, companies must regularly measure and analyze their sustainability performance using defined KPIs. Digital ESG tools play a key role in systematically recording data, identifying deviations early, and deriving optimisation measures.

- Regular data collection and analysis (e.g. CO2 emissions, water consumption, diversity indicators)

- Comparison with benchmarks and industry standards to classify your own ESG performance

- Internal audits and external ratings to objectively assess progress

- Dynamic adjustment of strategy if KPIs are not achieved or new opportunities arise

B. Adapting to new regulatory developments and market trends

Requirements for sustainable corporate governance are constantly evolving, driven by new ESG regulations, investor requirements and changing consumer preferences. Companies must remain flexible and proactively adapt their strategy.

| Driver | Examples |

|---|---|

| New regulatory requirements | Changed thresholds under the CSRD Omnibus, EU taxonomy changes |

| Market and competitive developments | Increasing demand for climate-neutral products |

| Technological innovations | New CO2 reduction technologies, digital ESG tools |

Companies that continuously measure, evaluate and adapt their strategy remain competitive and avoid regulatory risks.

Challenges and solutions

Developing and implementing a sustainability strategy comes with real challenges. These include growing regulatory requirements (CSRD, EU taxonomy), data collection burdens, internal process changes, and integrating ESG criteria into the corporate strategy.

Typical challenges

- Sustainability is treated as a side issue rather than a central component of business strategy

- Sustainability goals are not sufficiently linked to growth and innovation strategies

- Internal resistance when the focus is on short-term economic goals

- Difficulty identifying which ESG issues are truly strategically relevant

- Double materiality assessment is complex and requires interdisciplinary input

- Sustainability considerations are not integrated into investment and innovation decisions

- Unclear governance and responsibilities leave strategy ineffective

- No link between ESG targets and financial KPIs or remuneration models

Best practices for successful implementation

- Embed sustainability in corporate strategy: Link it to the corporate vision and long-term business goals; involve top management

- Identify material issues in a structured process: Use a double materiality assessment, involve stakeholders, and align with industry benchmarks

- Develop sustainable business models: Consider sustainability as an opportunity for new models such as the circular economy or sustainable services

- Clarify governance and responsibilities: Integrate sustainability into existing decision-making structures and create clear roles

- Link sustainability with financial targets: Connect ESG targets with financial KPIs; use ESG financing options such as green bonds

Our Excel-based materiality analysis template guides you through the double materiality assessment step by step, in line with CSRD and ESRS requirements.

Conclusion

For companies today, developing a sustainability strategy is a decisive success factor. Regulatory requirements such as the CSRD, rising stakeholder expectations and disruptive market changes make sustainable transformation unavoidable. Companies that strategically integrate sustainability into their business models benefit from competitive advantages, cost savings and improved financing options.

Frequently asked questions about developing a sustainability strategy

Who still needs to report under the CSRD after the Omnibus changes?

Since 18 March 2026, only companies with more than 1,000 employees AND more than €450m net turnover (both criteria must apply cumulatively) are required to report under the CSRD. Many companies that were previously in scope have now fallen outside the mandatory reporting obligation.

What is the difference between the four phases of sustainability strategy development?

The four phases are: (1) Analysis and target definition, where you identify ESG risks and opportunities through double materiality assessment; (2) Strategy formulation, where you link sustainability goals to your corporate strategy; (3) Implementation and reporting, where you translate goals into concrete measures and report under CSRD or voluntarily; and (4) Monitoring, where you measure ESG performance regularly and adapt to new requirements.

What is double materiality and why does it matter for strategy?

Double materiality covers two perspectives: financial materiality (how do ESG factors affect your company financially?) and impact materiality (how does your company affect the environment and society?). It is the core analytical tool of the CSRD and helps you identify which sustainability topics are truly relevant for your strategy, not just for compliance.

What can companies outside the CSRD scope do?

Companies with fewer than 1,000 employees or under €450m turnover are outside the mandatory CSRD scope. Many will choose to report voluntarily using the VS (Voluntary Standard), which is based on the VSME (EFRAG Dec 2024) and is being broadened to cover all companies outside the CSRD scope. CSRD-obligated companies may also not require value-chain partners with 1,000 employees or fewer to provide information beyond this voluntary standard.