Carbon Accounting

Perform carbon accounting according to the GHG Protocol. Which steps are particularly important? Which mistakes should be avoided?

As part of the CSRD (ESRS E1) and the VSME, companies are required to calculate and publish their carbon footprint. Other standards, such as the Global Reporting Initiative (GRI) and the International Sustainability Standards Board (ISSB), also require a carbon footprint.

The balance sheet is calculated by recording direct (Scope 1) and indirect (Scope 2 & 3) emissions, measured in CO₂ equivalents, along the value chain.

A credible and valid methodology for the calculation is indispensable. Both ISO 14064 and the GHG Protocol serve as a suitable and recognized framework for quantification.

Helpful tools for your carbon footprint and sustainability strategy

The best software solution for conducting the Double Materiality Assessment with AI support.

This Materiality Assessment template makes it easier for you to carry out and document your materiality assessment of the Scope 3 categories.

Practical 3-hour workshop on performing Scope 3 calculations. Physical or digital.

1. What is a carbon footprint?

A carbon footprint, also known as a greenhouse gas inventory, shows how many climate-damaging emissions a company causes directly and indirectly. All greenhouse gases according to the Kyoto Protocol are recorded along the entire value chain, expressed in CO₂ equivalents (CO₂e). Carbon accounting is usually carried out according to the international GHG Protocol and comprises three scopes.

Importance of the carbon footprint for companies

Carbon accounting is not only a legal requirement, but also serves other purposes:

- it makes a company’s quantitative climate impact transparent

- it forms the basis for identifying potential savings

- meeting legal requirements and stakeholder expectations

- obtaining improved financing options

- developing an effective sustainability strategy.

Basics and Standards

1. GHG Protocol (Greenhouse Gas Protocol)

The world’s most important and most frequently used standard.

It defines:

- the three emission areas (Scope 1, 2, and 3)

- methods for data collection and calculation

- clear rules for transparency and comparability

2. ISO 14064 / ISO 14067

International series of standards for the quantification and reporting of greenhouse gas emissions, which are particularly relevant if companies want a certifiable approach.

- ISO 14064-1: Corporate inventories

- ISO 14067: Product carbon footprints

3. Kyoto Protocol

Specifies which greenhouse gases must be taken into account (e.g., CO₂, CH₄, N₂O, HFCs, PFCs, SF₆, and often additionally NF₃).

These form the basis for all modern carbon accounting standards and are converted into emission factors.

4. IPCC Emission Factors (Intergovernmental Panel on Climate Change)

Scientific basis for:

- Global Warming Potentials (GWP)

- conversion of all greenhouse gases into CO₂ equivalents

Current GWP values are mostly taken from the IPCC Sixth Assessment Report (AR6).

The ESRS (European Sustainability Reporting Standards), including ESRS E1 on climate, are currently being revised. On 6 May 2026, the EU Commission published a draft of simplified standards for consultation. Key changes: mandatory data points cut by over 60%, total data points by over 70%, and a simplified materiality assessment. The revised standards are expected to be adopted around mid-2026.

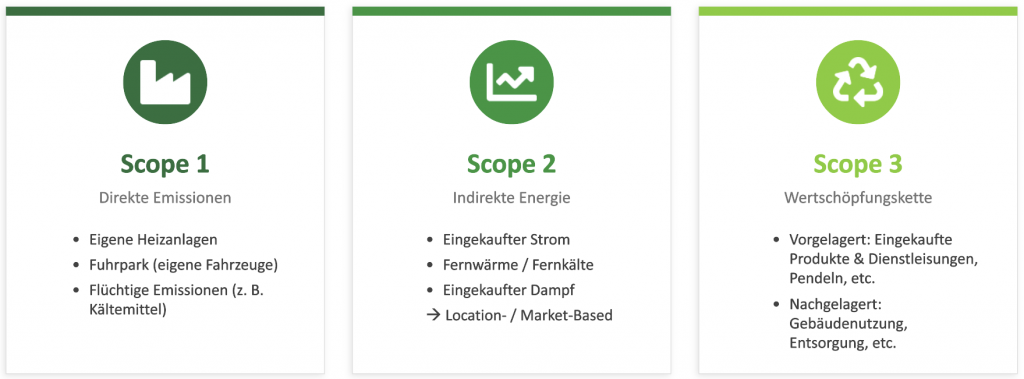

2. What do the three scopes mean?

The three scopes divide a company’s direct and indirect emissions. Scope 1 emissions are direct emissions such as a company’s own vehicles or heating systems; Scope 2 covers emissions from purchased electricity or heat; and Scope 3 includes indirect emissions, e.g., from upstream and downstream processes such as supply chains, business travel, or product use.

Scope 1: Direct emissions

Scope 1 includes all emissions that occur within the company itself. These include the combustion of fuels in own heating systems, machinery, or vehicles, as well as process-related emissions in production. These emissions are entirely under the company’s control.

Scope 2: Indirect emissions

Scope 2 includes emissions resulting from the consumption of purchased electricity, heat, cooling, or steam. They do not occur on the company’s premises but are caused because the company uses this energy.

Scope 3: Indirect emissions along the value chain

All other indirect emissions are covered by Scope 3, which often makes up the largest share of the total carbon footprint. This includes emissions from the production of purchased materials, transport and logistics, business travel, employee commuting, product use, and disposal. Scope 3 shows how strongly a company impacts the environment through its supply chains and product life cycles.

3. How is carbon accounting carried out?

The specific implementation of accounting is described in the GHG Protocol. In general, five principles must be observed:

- Relevance

- Transparency

- Consistency

- Completeness

- Validity/Accuracy

Step 1: Goal Setting

First, a clear definition of the accounting goals is crucial for effectively translating the results of a GHG inventory into climate protection measures. It determines the motivation behind the calculation, the period considered, and the base year (or comparison year) chosen. This allows priorities to be defined, progress to be measured, responsibilities to be clearly assigned, and investments to be targeted at the most effective levers.

Step 2: Define Organizational Boundaries & Approach

For a precise GHG inventory, the interaction between organizational boundaries and the approach is crucial. While organizational boundaries determine which parts of the company are included in the inventory, the chosen approach determines how these emissions are allocated.

Eigentumsanteilansatz Emissionen anteilig am wirtschaftlichen Eigentum (Equity Share) | Kontrollansatz | |

Finanzielle Kontrolle Beherrschender Einfluss auf die Finanz- und Geschäftspolitik | Operative Kontrolle Befugnis, die Betriebsabläufe zu steuern | |

Only the combination of both elements creates a consistent basis for evaluating emissions traceably within the corporate structure and assigning them to the correct scopes.

1. Equity Share Approach

In the Equity Share Approach, emissions are allocated according to a company’s economic ownership interest in an entity or operation. For example, if a company holds 40% of a joint venture, 40% of the emissions generated there are also attributed to it, regardless of whether it has operational or financial control. This approach provides a realistic picture of the emissions resulting from the company’s economic activities and is often used in corporate structures or by companies with multiple joint ventures.

2. Control Approach

2.1 Financial Control Approach

The Financial Control Approach allocates all emissions to the entities over which a company exercises financial control. Financial control means that the company has the authority to make financial and operational decisions. This is often the case through majority holdings or contractual arrangements. Even if the actual ownership share is lower, 100% of the emissions are recorded as soon as financial control exists. This approach ensures consistency in reporting and realistically reflects corporate decision-making and influence.

2.2 Operational Control Approach

The Operational Control Approach is about whether a company exercises operational control over an activity or facility. It is therefore about whether it can control the operational processes and environmental performance. A company has operational control if it directs the day-to-day operation of a facility or activity. This includes:

- Responsibility for procedures, safety standards, work processes, and environmental performance.

- The company can determine how activities are carried out, regardless of who owns the facility.

If a company manages the day-to-day operation of a facility, 100% of that entity’s emissions are attributed to it, even if ownership lies partially or fully with third parties. This approach is particularly practical as it takes into account those emissions that a company can actually influence in its daily operations.

Based on the chosen approach, Scope 1 & 2 emissions are allocated and calculated. Depending on the approach, there may be a shift between scopes and different results. The approach should be continued consistently for Scope 3.

Step 3: Scope 3 - Materiality Assessment

Since Scope 3 emissions often account for the largest share of the total greenhouse gas inventory and come from a variety of different sources that are not always relevant in their entirety for every company, a Materiality Assessment is carried out.

The aim of this analysis is to determine which of the 15 Scope 3 categories are actually relevant and material for the company. Note: This is not to be confused with the Double Materiality Assessment as a basis for CSRD reporting.

The categories where significant emission volumes arise or where significant influence exists are filtered out. A traceable evaluation and documentation of the selection is crucial, considering factors such as emission levels, data accessibility, influence possibilities, and relevance for stakeholders. This ensures that accounting remains efficient and focuses on the areas that make the greatest contribution to the climate footprint and reduction potential.

The 15 categories are separated into upstream and downstream emissions:

- 3.1 Purchased goods and services

- 3.2 Capital goods, e.g., machinery, buildings

- 3.3 Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

- 3.4 Upstream transportation and distribution

- 3.5 Waste generated in operations

- 3.6 Business travel

- 3.7 Employee commuting

- 3.8 Upstream leased assets

- 3.9 Downstream transportation and distribution

- 3.10 Processing of sold products

- 3.11 Use of sold products

- 3.12 End-of-life treatment of sold products

- 3.13 Downstream leased assets

- 3.14 Franchises

- 3.15 Investments

Step 4: Data Collection & Calculation

Data collection and calculation form the foundation of a reliable GHG inventory. All relevant consumption, activity, and process data are recorded in a structured manner, such as energy consumption, materials, transport volumes, or business travel. This raw data is then converted into CO₂ equivalents using recognized emission factors. A systematic, transparent, and consistent approach creates a robust overview of the company’s actual emissions. Depending on the level of ambition and data availability, the following data types can be used. A combination of methods is also permissible if the data situation does not provide more specific data.

Data Types

| Data type | Explanation |

|---|---|

| Spend-based | Calculates emissions based on financial expenditure for a product or service. |

| Average data | Uses average activity data (e.g., average weight, transport distance, industry values). |

| Supplier-specific | Uses primary data from suppliers, i.e., actual specific emissions of the products or services. |

Step 5: Documentation

Traceable and transparent documentation is essential. This should be observed throughout the entire accounting process. Decisions, such as why certain Scope 3 categories are not material, must also be logically argued and transparently communicated. This also serves auditability.

4. What aids and tools are available?

Numerous aids and tools are available to companies for creating a GHG inventory, which significantly simplify the process. These include specialized emission calculation software solutions that record data, automatically assign emission factors, and generate reports. Many ESG software solutions also have modules for carbon accounting. These also help to collect data efficiently and, in particular, to systematically record Scope 3 emissions.

In addition, national emission factor catalogs provide reliable factors for the calculation. Furthermore, “guidelines” such as the GHG Protocol or ISO standards support a structured approach.

We are also happy to offer a Scope 3 Workshop tailored to your company, online or on-site.

5. Carbon accounting complete: What's next?

After completing the carbon footprint, the crucial next step begins: defining and implementing measures. First, the identified emission drivers are analyzed to derive targeted reduction potentials, for example through energy efficiency, procurement, mobility, or logistics. On this basis, companies can develop a climate strategy with clear goals

, priorities, and responsibilities. Frameworks and certifications such as SBTi can help. Equally important is transparent communication with employees, customers, and stakeholders to make progress visible and build acceptance for change. The inventory is then updated regularly to track developments, plan new measures, and work toward climate neutrality in the long term.

Further reading and links

- GHG Protocol

- DIN EN ISO 14064-1 Part 1: Specification with guidance at the organization level for quantification and reporting of greenhouse gas emissions and removals

- DIN EN ISO 14064-2 Part 2: Specification with guidance at the project level for quantification, monitoring and reporting of greenhouse gas emission reductions or removal enhancements

- DIN EN ISO 14064-3 Part 3: Specification with guidance for the verification and validation of greenhouse gas statements

- SBTi – Science Based Targets initiative

Our self-service solutions combine pragmatic simplicity with in-depth expert knowledge and make sustainability reporting quick and effective to implement. 🚀 Discover the right CSR tools now!

6. Frequently Asked Questions (FAQ)

What is a carbon footprint or GHG inventory?

A GHG (greenhouse gas) inventory or carbon footprint indicates the emissions caused by a company.

Why is carbon accounting important?

Sound carbon accounting can not only be a regulatory requirement but also form the basis for a successful climate strategy. It also provides transparency about a company’s activities and can appeal to a specific target group. Furthermore, it is increasingly being requested by lenders or other stakeholders.

Which legal requirements affect the GHG inventory?

In particular, the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS) oblige companies to calculate a GHG inventory and present it transparently in their reporting. However, publication of the GHG inventory is also required under voluntary standards such as the VSME. Note: the VSME is being broadened into the "VS (Voluntary Standard)", a delegated act expected later in 2026, which also covers non-SMEs with fewer than 1,000 employees that fall outside the CSRD scope.

What does material mean in the context of the GHG inventory?

The 15 Scope 3 categories must be assessed according to their materiality, and only these should be included in the inventory.

Can conclusions be drawn from the Double Materiality Assessment regarding Scope 3 categories?

The Double Materiality Assessment may provide a direction for the material Scope 3 categories, but it does not replace the structured analysis and assessment of the 15 Scope 3 categories.

What role does data availability play in the calculation?

The quality of the result depends on data availability. As soon as estimates or average values are used, the validity of the calculation decreases. However, in some cases not all data is available, so an estimate is unavoidable.

How can modern technologies like AI support GHG accounting?

AI-powered tools can analyze large amounts of data, identify patterns and trends, and thus speed up the process. AI acts as a supporting tool, while the final assessment should still be based on human expertise.

What are the advantages and disadvantages of specialized software compared to Excel?

Excel offers flexibility and is often sufficient for smaller projects. Specialized software solutions, on the other hand, offer advantages such as automated data integration, interactive visualizations (e.g., hotspot analysis of Scope 3 categories), and higher efficiency for complex analyses – which is particularly advantageous for large amounts of data and high quality standards.

How are stakeholders involved in the GHG process?

Companies can involve stakeholders in the process and data collection through regular analyses and surveys. Other stakeholders require the results of the GHG accounting, which is why attention should be paid to transparent and valid documentation and communication.

Which companies must report a GHG inventory under CSRD after the 2026 changes?

Since 18 March 2026, the Omnibus package has narrowed the CSRD scope. Companies must now exceed both thresholds cumulatively: more than 1,000 employees and more than €450 million net turnover. Companies that fall below either threshold are no longer obligated under CSRD. Many of them choose to report voluntarily using the VSME (or the forthcoming VS).

How can CSR-Tools support me?

We are happy to support you in calculating your GHG inventory, for example through a Scope 3 workshop, our tools and templates, or individual consulting. Please feel free to contact us.