Sustainability report: Who takes on the key roles?

Find out which departments are responsible for the sustainability report and how you can optimize your processes.

- Responsibility for the sustainability report is spread across multiple departments. It is a genuine team effort.

- The Management Board carries ultimate legal responsibility. The Supervisory Board monitors quality and selects auditors.

- In practice, Accounting and the Sustainability department share coordination most often.

- Clear role definitions, early data collection, and efficient tools make the process significantly smoother.

- Under the revised Omnibus thresholds (in force since March 2026), only companies with more than 1,000 employees AND more than €450m net turnover are obligated to report.

The CSRD thresholds have changed. Since 18 March 2026, reporting is only mandatory for companies with more than 1,000 employees AND more than €450m net turnover (both criteria must be met). Many companies that expected to report are no longer in scope. For the full picture, read our article on CSRD Omnibus - What the EU proposal means for companies.

The increasing requirements of the Corporate Sustainability Reporting Directive (CSRD) leave companies with a practical question: who is actually responsible for the sustainability report and the preparation of the double materiality assessment? The answer is complex, because it is a real joint task. In this article, you will find out which internal and external stakeholders are typically involved, how responsibilities are allocated, and how you can make the sustainability reporting process more efficient.

1. Responsibility within the company

Management Board and Supervisory Board

Overall responsibility for the sustainability report, which forms part of the management report, lies with the Management Board. It must ensure that the report complies with legal requirements and reflects the company's strategic priorities. The Supervisory Board monitors the quality of the report and, if necessary, selects external auditors.

Specialist departments: a cross-departmental task

Implementing the sustainability report is a cross-team challenge. Various departments play a central role:

- Sustainability department: Often the main coordinator for collecting and analyzing relevant data.

- Finance/Accounting: Provides methodological support, particularly for integrating financial and non-financial information.

- Legal/Compliance: Helps meet regulatory requirements and ensures the legal conformity of the report.

- HR: Provides data on social topics such as diversity, working conditions, and personnel development.

- Risk management: Assesses sustainability risks and their impact on business strategy.

- Marketing/Communication/Investor Relations: Presents complex topics in a way that is easy to understand for a broad target group.

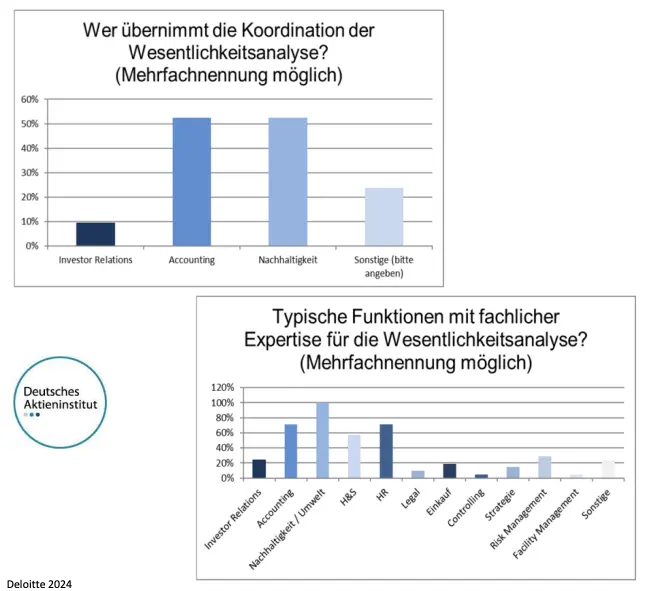

2. Insights from the field: who takes care of the materiality assessment

A recent study by Deutsches Aktieninstitut shows how companies in practice divide tasks relating to the sustainability report and the materiality assessment. Note: multiple answers were possible.

Coordination of materiality assessment:

| Department | Share of companies |

|---|---|

| Accounting department | ~50% |

| Sustainability department | ~50% |

| Individual solutions (e.g. dedicated project teams) | ~20% |

Technical expertise for materiality assessment:

| Department | Share of companies |

|---|---|

| Sustainability department | More than 80% |

| Accounting team | Around 60% |

| Legal, HR, Compliance, Risk Management | Notable contributions |

This data underlines that the sustainability report is a joint task requiring different perspectives and competencies. It is also notable how differently responsibilities are distributed within companies, and that many companies have not yet set up a dedicated department for the materiality assessment.

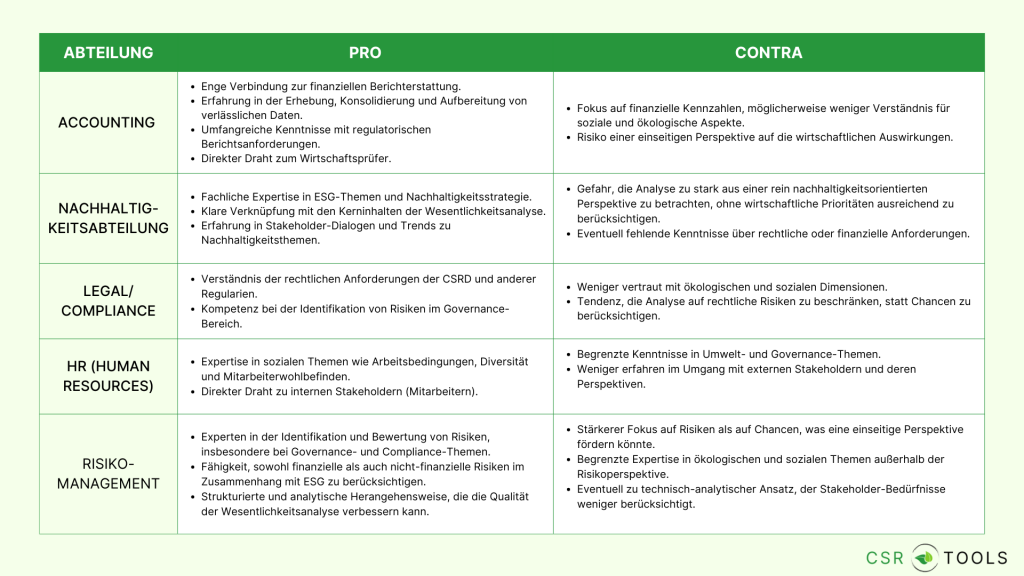

Best practice from our experience

From our perspective, the "CSRD" task should be assigned as closely as possible to the Finance and Accounting team. We see the following advantages:

- Close link to financial reporting to publish a uniform and consistent management report

- Experience in collecting, consolidating, and preparing reliable data

- Extensive knowledge of regulatory reporting requirements

- Direct line to auditors and experience in working with them

The following graphic shows other important points for considering which department is best suited to this task.

3. External partners for the sustainability report

In addition to internal stakeholders, external partners also play a central role:

- Sustainability consultants: CSRD experts contribute specialist knowledge on the European Sustainability Reporting Standards (ESRS) and provide support with the materiality assessment.

- Auditor: The CSRD requires an external audit of sustainability reports to ensure quality and transparency.

4. Tips for an effective materiality assessment

Many companies work with limited resources on the sustainability report. Allocating those resources well is especially important when the task falls to departments with other primary responsibilities. The following tips can make the process smoother:

- Define clear responsibilities early. Decide which department takes on which role from the start. Clear coordination minimizes misunderstandings and promotes efficiency.

- Promote cross-departmental cooperation. Workshops and internal training create a better shared understanding of CSRD requirements and improve collaboration.

- Start collecting data early enough. When many departments are involved, gathering the necessary data is a major task. Depending on the size of your company, it may be sensible to start before the actual reporting year begins.

- Use efficient tools. With our Excel template for the double materiality assessment you can maintain an overview. It helps you document the results of your materiality assessment in a structured way and simplifies the preparation of the sustainability report. If you prefer a web-based software solution, we can highly recommend the Materiality Master.

- Take advantage of external support. Consultants and auditors can help you overcome challenges and meet regulatory requirements. We offer a practice-oriented 4-hour workshop on the topic of the materiality assessment, which will prepare you well for this part of your sustainability reporting.

Structure your double materiality assessment with a ready-to-use Excel template. Document all relevant topics, assign impact and financial materiality, and generate a clear overview for your report.

5. Conclusion: The sustainability report as a team effort

Preparing a sustainability report requires the interaction of many players. Cross-departmental collaboration, supported by clear processes and efficient tools, is the key to success. Companies that start planning early and deploy suitable resources can meet the requirements and gain valuable insights for their business strategy at the same time.

Frequently asked questions about sustainability report roles

Who is ultimately responsible for the sustainability report?

Ultimate responsibility lies with the Management Board. The sustainability report forms part of the management report, so the Board must ensure it meets legal requirements and reflects the company's strategy. The Supervisory Board monitors quality and, where needed, selects external auditors.

Which department typically leads the materiality assessment?

In practice, Accounting and the Sustainability department share the coordination role most often, each handling it in around 50% of companies. For technical expertise, more than 80% of companies involve the Sustainability department, while around 60% rely on the Accounting team. Many companies also draw on Legal, HR, Compliance, and Risk Management.

Does my company still need to produce a CSRD sustainability report after the Omnibus changes?

Since 18 March 2026, reporting is only mandatory for companies with more than 1,000 employees AND more than €450m net turnover. Both criteria must be met. Many companies that previously expected to report no longer fall within scope. If you are just outside the threshold, the VSME voluntary standard (which is being broadened into the "VS - Voluntary Standard") offers a lighter framework to communicate your sustainability performance to customers and investors.

What tools can help with the materiality assessment?

For an Excel-based approach, our materiality analysis template provides a structured way to document your results. For a web-based solution, the Materiality Master is worth considering. We also offer a 4-hour practical workshop for teams that want hands-on guidance through the process.