- On March 25, 2025, we held a practice-oriented VSME webinar with audit.innovation that drew more than 170 live participants.

- This page contains the recording, the downloadable presentation, and answers to all participant questions.

- The VSME is a voluntary standard; no audit or xBRL tagging is required.

- A Double Materiality Assessment is not mandatory for VSME but is strongly recommended as a strategic tool.

- The VSME standard is being broadened into the "VS (Voluntary Standard)", which will also cover non-SMEs outside the CSRD scope.

On March 25, 2025, we held a practice-oriented VSME webinar together with the auditing firm audit.innovation. More than 170 participants followed live how we clarified the most important questions about the voluntary sustainability report. Topics ranged from the relevance of the VSME standard in the context of CSRD to the role of the Materiality Analysis and concrete implementation steps.

In this article you will find the recording of the webinar, the presentation for download, a FAQ section with all participant questions, and further helpful links and tips for your own VSME reporting.

VSME Webinar: Recording

Presentation of the VSME webinar

The slides shown during the ESRS VSME webinar can be downloaded for free.

Answers to your questions at the VSME webinar

Numerous participants asked questions in the VSME webinar. Unfortunately, we were not able to answer all questions live. We are therefore making all our answers publicly available below.

Questions about the VSME standard

How does the VSME standard fit in with the SBTi (Science Based Targets initiative)?

The VSME can serve as an introduction to structured sustainability reporting, while SBTi specifies concrete science-based climate targets. SBTi-compliant targets can be specified in disclosure item C3 "GHG reduction targets and climate transformation" of the comprehensive module. Both initiatives complement each other. The VSME creates transparency; SBTi defines ambitious reduction targets.

Are there already companies that report in accordance with VSME?

We have not yet seen any officially published reports based on the final VSME standard. But the first applications are underway, especially among companies that want to report voluntarily or prepare a test report before they become subject to reporting under the Corporate Sustainability Reporting Directive (CSRD). Practical examples can be expected in the next 3-12 months.

When will the VSME "Plus" be published? Is there any information on this?

It is currently unclear whether a "VSME Plus" will be released. The name is partly used speculatively to describe a possible further development. So far, there is no official information from EFRAG or the EU Commission on a "Plus" version.

What is confirmed: the VSME standard is being broadened into the "VS (Voluntary Standard)" via a delegated act expected later in 2026. The VS is based on the VSME (EFRAG December 2024) with small content adjustments. Importantly, the VS will cover not just SMEs but all companies with fewer than 1,000 employees (or under 450 million euro turnover) that fall outside the CSRD scope. If there is further news, we will report on it in the CSRD Compass newsletter.

Isn't national implementation (e.g. in Germany) more important than the European requirement?

As the VSME is voluntary in nature, it is not expected to be transposed into national law.

Both levels are important for companies subject to CSRD that have to report in accordance with the comprehensive ESRS. It is a European requirement, but its implementation takes place via national law (in Germany, for example, via the German Commercial Code). It is therefore crucial to understand the EU requirements, but also to keep an eye on specific national interpretations and deadlines.

Does it make sense to report voluntarily on an ESRS basis, or is VSME the better choice?

If companies are subject to CSRD reporting requirements, there are advantages to reporting voluntarily in accordance with the comprehensive European Sustainability Reporting Standards (ESRS) at an earlier stage. As the EU Commission has announced its intention to revise the ESRS as part of the omnibus proposal, we recommend implementing the VSME report for the time being in order to avoid duplication of work. As the changes to the ESRS are still being finalised, voluntary implementation of the full ESRS may mean unnecessary additional work.

For companies without a CSRD obligation, the VSME standard is the more sensible and pragmatic solution. It is much leaner, with no management report obligation and no audit obligation.

Does the basic module relate only to your own company and the comprehensive module to the supply chain?

Not quite. Both modules can contain information on the supply chain, but the level of detail in the comprehensive module is higher. The comprehensive module covers more ESG topics in greater depth, sometimes also with reference to upstream or downstream activities. In general, information on the upstream and downstream value chain is significantly less pronounced in the VSME than in the comprehensive ESRS.

Do I have to do xBRL tagging with VSME?

No. xBRL tagging is mandatory for CSRD reporting, but not for the voluntary VSME standard. There is (still) no digital submission obligation.

Our company is not subject to CSRD reporting until 2028. Can we start with the VSME in advance?

Yes, provided the company is not already required to report under the Non Financial Reporting Directive (NFRD). The VSME report is a voluntary standard and can be used regardless of the size of the company. The VSME is a good starting point, especially for companies that want to prepare for the comprehensive CSRD reporting obligation.

To best prepare for the upcoming reporting obligations, we expressly recommend carrying out the Double Materiality Assessment even if you are initially only reporting in accordance with VSME.

Do you have to report on Scope 3 emissions in the comprehensive module?

Scope 3 is not included in the basic module. Scope 3 disclosures are optional in the comprehensive module. Whether they are relevant depends on the business model. If Scope 3 is material, it should be reported.

Can we include additional topics in the VSME report that emerge from the DMA as relevant?

Yes, according to paragraph 10 of the VSME, the inclusion of information not covered by the VSME is even expressly desired. This ensures that the report actually covers the points described in paragraph 9, such as relevance or comparability.

Does the VSME advise against carrying out a Materiality Assessment?

The current version of the VSME update from December 2024 no longer requires a Materiality Assessment to comply with the standard. However, explicitly discouraging it is beyond what the standard says. On the contrary, conducting a Materiality Assessment, even if only initially as a "light version", is always recommended.

The DMA serves as a central element for risk planning and long-term strategy development. In addition, some data points within the VSME can already be answered with the help of the DMA, making the DMA a very helpful tool for VSME reporting.

Questions about the VSME data points list and the VSME report template

How do I get the VSME data points list?

The VSME data point list can be purchased from us in the online store or by e-mail order on account. You also receive the data point list free of charge when you purchase the VSME report template.

If there are any updates to the VSME standard, the list of VSME data points will be updated accordingly.

Is it possible to purchase the VSME report template as a license model (for consulting use)?

Yes, we offer a license model for consulting firms and auditing companies, which also applies to the VSME report template. You are welcome to arrange a non-binding introductory meeting with us to discuss further details.

Can the Materiality Assessment Excel template from CSR Tools be adapted to VSME?

Yes, the Excel template for performing the Double Materiality Assessment from CSR Tools can be used for the VSME standard.

For a VSME-compliant application, the relevant ESG topics and disclosure requirements from the VSME standard can be mapped to the ESRS topics in an integrated manner (see also VSME mapping). This makes it possible to determine which content from the VSME is important for your company and which data points should be included in the report. If you have specific questions, you can contact us via the support chat or by e-mail.

We are also working on a template for a "Light" Materiality Analysis that is ideally suited to the VSME standard. A DMA Light module is also being added to the Materiality Master materiality analysis software.

Ready-to-use Word template for your VSME sustainability report. Includes all required data points and a free copy of the VSME data points list.

Questions about the audit or for the auditors

Can individual key figures such as the corporate carbon footprint (CCF) also be audited by external auditors?

Yes, an individual audit of specific quantitative disclosures such as the CCF is possible. Auditors accept such audit opinions as a basis, especially for non-financial key figures, provided the third party commissioned is suitably qualified and reliable. This can reduce the overall cost of a subsequent VSME or CSRD audit, as values that have already been audited do not have to be audited again.

Important: the methodology and traceability of the calculation must be documented.

What role do certification institutes still play today?

Certification bodies retain an important role, albeit in addition to reporting. They can validate data, processes or management systems (e.g. ISO 14001 for environmental management or ISO 50001 for energy). ISO certifications also facilitate compliance with the CSRD/ESRS.

These certificates increase the credibility of the reporting but do not replace a structured VSME/CSRD reporting obligation.

Does a VSME report have to be audited by an auditor?

The VSME is a voluntary standard; there is no statutory audit requirement. An audit by an auditing firm or another auditing company is optional, but can create confidence among stakeholders. Your stakeholders may also require validation of the VSME report by a third party.

As an alternative to a traditional audit, a plausibility assessment (certificate in accordance with IDW S7) without a comprehensive audit by an auditor could be useful.

Can both VSME and ESRS be used in a group?

Yes, this is generally possible. If a group is subject to CSRD for the parent company (ESRS), but a subsidiary wishes to report voluntarily, it can apply the VSME standard. It is important to make transparent in the group consolidation which standard each company has reported in accordance with.

Can a subsidiary that is exempt from the CSRD reporting obligation (due to group consolidation) respond to requests voluntarily in accordance with VSME?

An exempt subsidiary does not have to publish its own report in accordance with ESRS. However, it can voluntarily provide information in response to external requests, for example on the basis of the VSME standard. This is a pragmatic way of creating transparency without having to map the full complexity of ESRS.

As a rule, there is no legal entitlement to complete ESRS information unless there are contractual or regulatory obligations, e.g. along the supply chain.

Other questions from the VSME webinar

Is the 1,000-employee limit calculated including affiliated companies?

Yes, the number of employees refers to the consolidated level, including subsidiaries and other affiliated companies. The decisive factor is the so-called group reference according to group accounting. A company with 600 employees of its own may still be subject to reporting requirements if the entire group has more than 1,000 employees.

Can the goal of CSRD, promoting sustainable economic development, still realistically be achieved?

In principle, yes. The CSRD can make an important contribution to more sustainable corporate governance, above all through uniform requirements, greater transparency and better comparability. However, with the omnibus proposal in February 2025, the EU itself recognised that the original scope of application was too broad.

By postponing the reporting obligation for many large companies, the group of affected companies has been significantly reduced. This reduces the impact in the short term, but it increases acceptance and feasibility, particularly for smaller and medium-sized companies, and could place a greater focus on implementing sustainability projects rather than fulfilling the reporting obligation.

If the remaining companies see reporting not only as an obligation but also as a strategic tool, the original goal of promoting sustainable economic development can be achieved in a realistic and practical manner.

VSME Webinar: Survey results

As part of the webinar, we involved the participants interactively and asked them about their level of knowledge, their need for support and how they deal with Materiality Assessment.

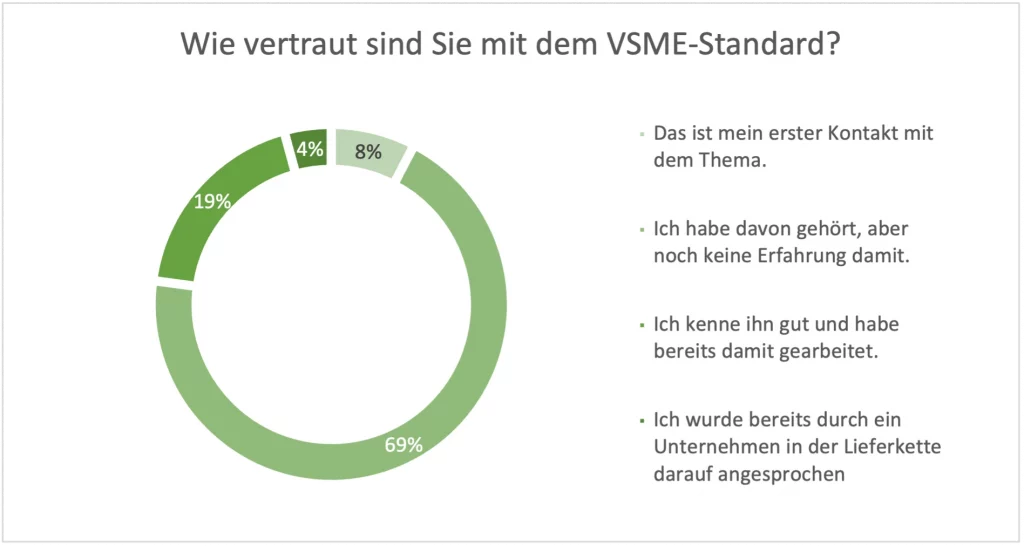

The majority of webinar participants are still at the beginning: 69% stated that they had already heard of VSME but had no experience of it. For 8%, the webinar was even their first point of contact with the topic. This shows clearly that the need for guidance, practical explanations and introductory aids remains high.

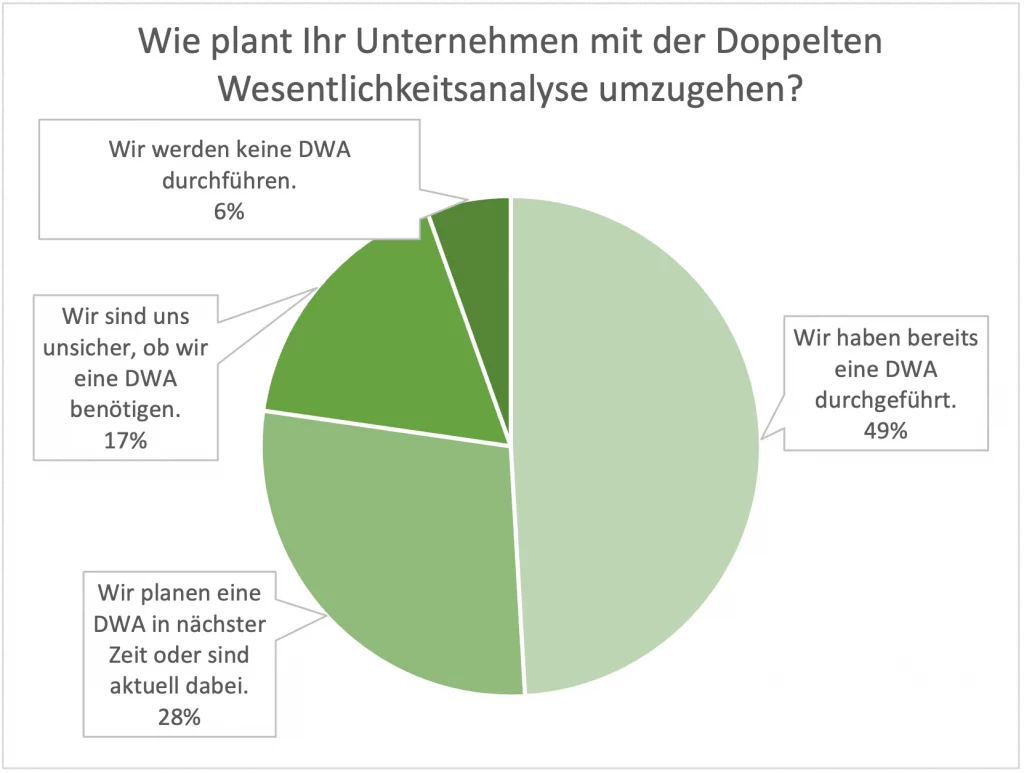

Almost half of the participants (49%) have already carried out a Double Materiality Analysis. A further 28% are currently implementing or planning to do so. Only 6% exclude the DMA completely. This underlines the high relevance of dual materiality, also in the context of the VSME, where it is not mandatory but makes strategic sense.

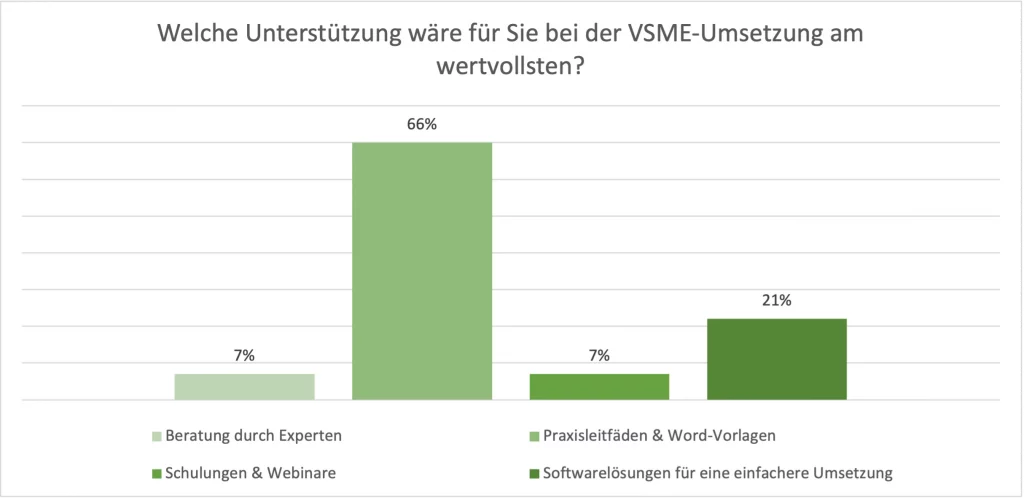

Practical guides and templates are by far the most requested tools: 66% of participants named them as the most valuable support. They are followed by ESG software solutions (21%), while individual CSRD advice or training were only mentioned by 7% of webinar participants. The desire for pragmatic, immediately applicable CSRD tools is clearly recognisable.

Other links and notes from the VSME webinar

In the VSME webinar, we referred to further sources and helpful links:

- Official VSME Reporting Standard of EFRAG

- Unofficial German translation of the VSME standard

- Essentially no objection - The Audit Podcast

- GHG Protocol Standards & Guidance

- VSME: Mapping of the main ESRS topics

- AI prompts for the VSME report

- VSME report template (Word)

- List of VSME data points

Frequently asked questions about the VSME webinar

Who is the VSME standard relevant for?

The VSME (Voluntary SME Standard) was designed for small and medium-sized enterprises that want to report voluntarily. As of 2026, it is being broadened into the "VS (Voluntary Standard)" to also cover non-SMEs with fewer than 1,000 employees or under 450 million euro turnover that fall outside the CSRD scope. Companies subject to the CSRD may not require value-chain partners with 1,000 employees or fewer to provide information beyond this voluntary standard.

Is a Double Materiality Assessment required for VSME reporting?

No, the current VSME standard does not require a materiality assessment for compliance. However, we strongly recommend carrying one out, even as a light version. The DMA helps you identify relevant risks and opportunities, can answer several VSME data points directly, and forms a solid foundation if you later move to full CSRD reporting.

Does a VSME report need to be audited?

No. The VSME is a voluntary standard and there is no statutory audit requirement. An audit by an auditing firm is optional but can increase stakeholder confidence. As an alternative to a full audit, a plausibility assessment (certificate in accordance with IDW S7) may be a practical option.

Can we use the CSR Tools Materiality Assessment template for VSME?

Yes. The Excel template for the Double Materiality Assessment from CSR Tools can be used for the VSME standard. The relevant VSME topics can be mapped to ESRS topics in an integrated manner, helping you determine which data points are relevant for your company. A dedicated VSME Mapping file is also available separately.